Principal

Revitalization Partners

With COVID-19 causing a drastic decline in revenues for many businesses, lenders have made a number of accommodations for non-performing loans, particularly through short-term deferrals. However, as the pandemic rages on, Bill Lawrence explains why lenders need to be proactive to avoid risk.

Since the beginning of the COVID-19 crisis, the Federal Reserve has taken swift action to provide tools to help banks cope with this anticipated increase in non-performing loans. One of the most sweeping programs, which was aimed at helping small- to medium-sized businesses early in the COVID-19 crisis, was the deferred payment program. If borrowers could not make monthly loan payments, lenders could initially defer those obligations for a three-month period. The deferral period ultimately could be extended to six months or longer based on the lender’s discretion.

While the program was responsible for saving thousands of businesses in the short term, its continuation has created significantly increased exposure for participating lenders. According to a Bloomberg report from August, as borrowers struggled with the effects of the first few months of the COVID-19 pandemic, the amount of deferred loans at Bank of America, Citigroup, JPMorgan Chase and Wells Fargo exceeded $150 million.1 Bloomberg further noted that “the same banks set aside more than $32 billion for loan losses in the second quarter of this year.” The towering number of deferred loan payments, combined with the near record level of increased loan loss reserves in a single quarter, signal that relief programs may not be enough to deal with the tsunami that is forming.

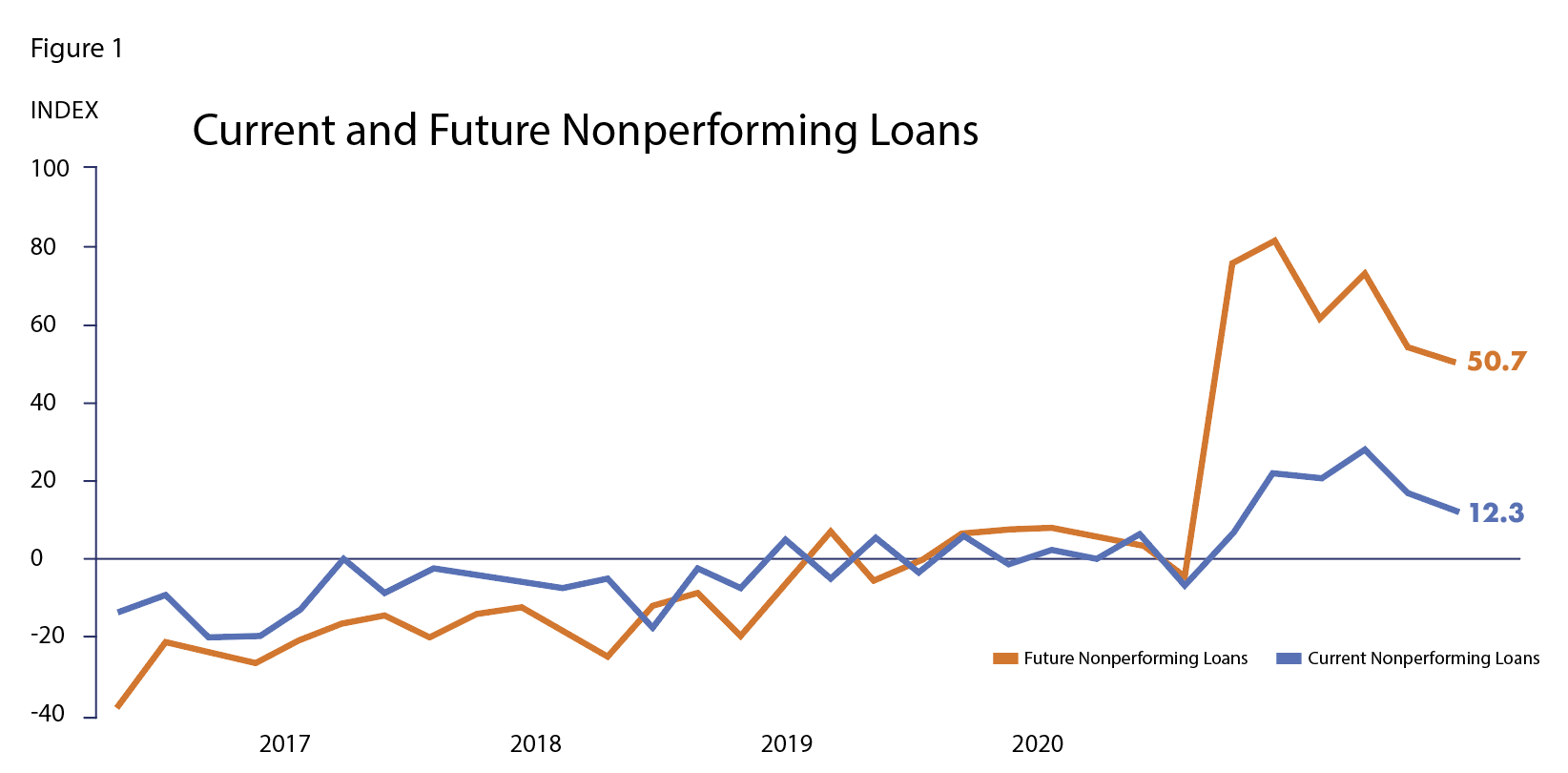

Domestic banks’ concerns over the threat was initially revealed in a survey conducted in May by the Federal Reserve Bank of Dallas. Findings showed that 83% of financial institutions expected an increase in non-performing loans within six months, while 27% reported an increase in non-performing loans during the preceding six weeks. Data from a recent November 2020 survey confirmed those threats by reporting an alarming increase in current and future nonperforming loans (see Figure 1).

Because of the magnitude of troubled credits, commercial lenders should be extra vigilant and not wait for loan deferral programs to end before taking action to mitigate loan write-downs. All lenders have tools to continually evaluate and score the creditworthiness of their commercial borrowers. However, there is a risk that the usual warning signs raised by these methods will be somewhat neutralized or minimized by the availability of the current loan deferral programs.

While actions may be taken to exit or foreclose on the worst of the worst loans in a lender’s deferred payment program, this represents a small fraction of the loans. Most businesses in the portfolio, however, will likely continue to operate, and if appropriate action to mitigate cash flow losses is not taken, they will reach a point of no return. At that juncture, they will never be able to repay the loan in full and the lender will be faced with writing off a portion — if not the entire loan — as a loss.

Source: Federal Reserve Bank of Dallas – November 2020 Banking Conditions Survey

Preemptive Measures

Further, lenders should require that management outline steps being taken to mitigate cash flow declines and insist on monitoring the progress the company makes in achieving its goals. While businesses may resist this added oversight, it should be a condition of acceptance into a loan deferral program, or, at a minimum, be implemented if loan deferrals are required beyond the initially agreed upon period.

Resetting Expectations

The need for this increased oversight becomes even more important since it appears that the end of the COVID-19 crisis is farther away than many originally thought. Eric Rosengren, president of the Boston Federal Reserve Bank, said that increasing COVID-19 cases and a rise in bankruptcies could lead to “a possible credit crunch,” according to CME Group.2 His warning underscores the fact that lenders must be proactive and act sooner, rather than later, to mitigate risk. Time is running out.

-

P. Lubbers, “Biggest U.S. Banks Have More Than $150 Billion of Deferred Loans,” Bloomberg, Aug. 2020

-

CME Group, “US: Boston Federal Reserve Bank President Eric Rosengren Speech,” CME Group, Sept. 2020

Bill Lawrence is a principal at Seattle-based restructuring and corporate advisory firm Revitalization Partners. He and his partners write regularly about the operational and financial challenges companies face in successfully restructuring companies.