The $1.8 trillion private credit market is experiencing its most severe liquidity test since the asset class emerged as a dominant force in middle market finance. A cascading series of redemption events across some of the industry’s most prominent funds has exposed a structural vulnerability that many market participants had dismissed as theoretical: the mismatch between investor expectations of liquidity and the inherently illiquid nature of the underlying loan portfolios.

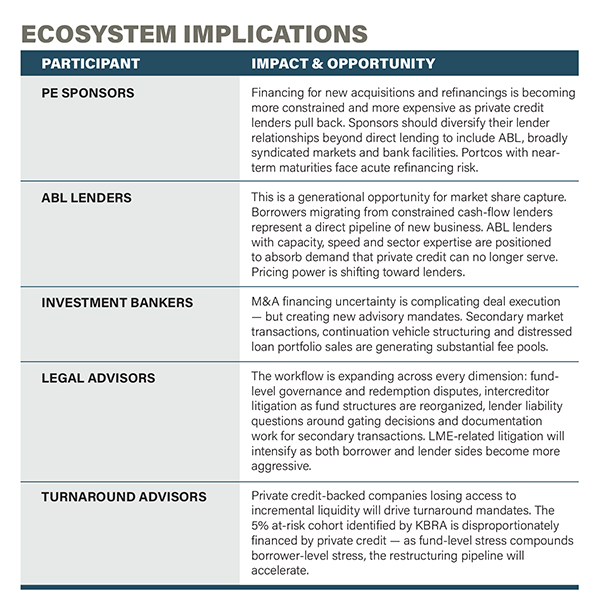

For the middle market dealmaker ecosystem — from PE sponsors dependent on private credit financing to ABL lenders positioned to absorb displaced demand — the implications extend far beyond any single fund’s liquidity challenges. The redemption wave is reshaping the competitive landscape for middle market lending, altering the terms available to borrowers, and creating a new category of distressed opportunity for sophisticated participants.

The Timeline of Contagion

The current crisis has a clear patient zero. In November 2025, Blue Owl Capital announced plans to merge its non-traded BDC, OBDC II — a $1.7 billion vehicle focused on senior secured lending to U.S. middle market companies — with its larger, publicly traded OBDC fund, in response to mounting redemption pressure.1 The proposed merger would have imposed an approximately 20% haircut on OBDC II investors. Shareholders revolted, the proposal was shelved and the fund ultimately suspended regular redemptions permanently, pivoting instead to periodic payouts funded by asset sales.2

What followed was a classic contagion pattern. At Blackstone’s BCRED, investors sought to withdraw $3.8 billion, representing 7.9% of net assets. Blackstone took the extraordinary step of committing $400 million from its own balance sheet and senior executives’ personal capital to satisfy all requests.3 The gesture of confidence did not contain the spreading anxiety.

The contagion accelerated through March 2026. Cliffwater’s $33 billion flagship private credit fund received withdrawal requests for 7% of assets. BlackRock restricted withdrawals on its $26 billion HPS Lending Fund. Morgan Stanley capped payouts on its $7.6 billion North Haven Private Income Fund at 5% despite receiving requests for 10.9% of shares. Stone Ridge Asset Management announced it would fulfill only 11% of redemption requests in its LENDX fund, a vehicle heavily exposed to Buy Now, Pay Later and fintech-originated consumer loans.3,4

The aggregate numbers are staggering. Investors requested more than $10 billion in redemptions from private credit funds in Q1/26 alone, and Goldman Sachs projects total fund asset reductions of $45 billion to $70 billion over the next two years if retail investor outflows continue.5

The Structural Root Cause: Semi-Liquid Meets Illiquid

The fundamental problem is architectural, not cyclical. Private credit funds historically raised capital through closed-end structures with defined terms — investors committed capital for long periods, matching the illiquid nature of the underlying loan portfolios. This structure insulated funds from redemption pressure and allowed them to capture an illiquidity premium.

The industry’s aggressive push into retail wealth channels over the past several years changed the equation. Products designed for institutional investors were repackaged as semi-liquid vehicles for individual investors, offering quarterly or monthly redemption windows.6 The retail investors attracted by high yields proved far less patient than the institutional allocators who traditionally anchored private credit funds. When headlines about fund stress emerged, the rush for exits overwhelmed the limited liquidity mechanisms these structures provided.

The irony is acute: the very liquidity features designed to attract retail capital became the vector for destabilization. As one senior analyst at Oppenheimer said to CNBC, redemption limits in private credit structures are designed as protective features — the funds invest in illiquid loans intended to be held to maturity, and liquidity constraints prevent forced sales at distressed prices.5 But when multiple funds simultaneously face redemption pressure, the protective mechanism transforms into a confidence-eroding signal.

The Middle Market Lending Impact

For middle market borrowers, the most immediate consequence is tighter financing availability. Private credit’s rapid growth was fueled in part by borrower-friendly terms: covenant-lite structures, aggressive leverage multiples and speed of execution that traditional bank lenders could not match. As funds face capital constraints and heightened scrutiny, those terms are recalibrating.

One restructuring partner at a major law firm captured the shift in an interview with Middle Market Growth: the market is coming back to covenants.5 For borrowers accustomed to cash-flow-based facilities with minimal financial maintenance tests, the return to traditional covenant packages represents a significant adjustment. For lenders — particularly ABL shops that never abandoned collateral-based underwriting discipline — it represents validation of a business model that prioritizes asset protection over enterprise value narratives.

Credit Quality Under the Surface

The redemption crisis is unfolding against a backdrop of deteriorating borrower health that private credit’s headline metrics have partially obscured. KBRA’s Q4/25 surveillance of 2,416 unique middle market sponsored borrowers found that while the median remained stable, the margins are under increasing stress: 19% of borrowers reported declining sales, 22% reported declining EBITDA and multilevel downgrades surged 2.9 times quarter over quarter.7

The shadow default rate — capturing companies showing clear economic distress despite technical covenant compliance — more than doubled from 2.5% in Q4/21 to 6.4% in Q4/25.7 Fitch Ratings reported the private credit default rate climbed to 5.7% on a trailing 12-month basis, the highest level recorded since February 2025.9 When headline metrics diverge this significantly from underlying economic reality, the eventual reconciliation tends to be abrupt.

The Bifurcation: Originators vs. Distributors

A critical structural shift is emerging within private credit itself. The market is bifurcating between those that can originate loans and those that can move them into durable funding channels — warehousing facilities, CLO structures, whole loan sales and other distribution mechanisms.10 Funds reliant on semi-liquid vehicle capital are discovering that origination capability alone is insufficient if the funding base is unstable. Managers with diversified capital sources — including permanent capital vehicles, separate accounts and institutional commitments — are better positioned to maintain lending activity through the current stress cycle.

The Secondary Market as Relief Valve

The secondary market for private credit interests is emerging as the primary mechanism for resolving the liquidity mismatch. Activist investors and specialized secondary funds are positioning to purchase stakes from investors seeking exits. Saba Capital, led by Boaz Weinstein, launched tender offers to buy stakes in several private debt vehicles, including Blue Owl-managed funds.5

Houlihan Lokey has been an early mover in structuring continuation vehicles as liquidity solutions for private credit funds under redemption pressure. The firm’s view, as reported by Fortune, is that CVs represent an underpriced option that could prevent significant NAV declines by allowing departing investors to achieve full liquidity while replacement investors take positions at modest discounts.3

The constraint is scale. The private credit market represents approximately $1.8 trillion in assets; the secondary market totals roughly $200 billion, divided roughly evenly between equity and credit secondaries.3 If redemption pressure intensifies materially beyond current levels, it remains unclear whether secondary market capacity can fully absorb the selling. However, market participants note that new capital is flowing into secondary strategies specifically to exploit the dislocation, creating a self-reinforcing dynamic that may expand capacity in real time.

What Comes Next

The private credit redemption cycle is unlikely to resolve quickly. The structural mismatch between retail investor expectations and private credit’s inherent illiquidity will require either a substantial repricing of semi-liquid fund terms, a shift back toward institutional- only vehicles, or the development of robust secondary market infrastructure that provides genuine liquidity without destabilizing fund portfolios.

For the middle market, the most consequential outcome may be a permanent recalibration of the lending landscape. The era in which private credit was the default — and often the only — source of middle market acquisition financing is giving way to a more diversified capital markets environment where ABL, broadly syndicated lending and bank facilities compete alongside direct lenders for borrower relationships. That competition, while disruptive in the near term, may ultimately produce a healthier financing ecosystem for middle-market companies and the dealmakers who serve them. •

Rita E. Garwood is editor in chief of ABF Journal.