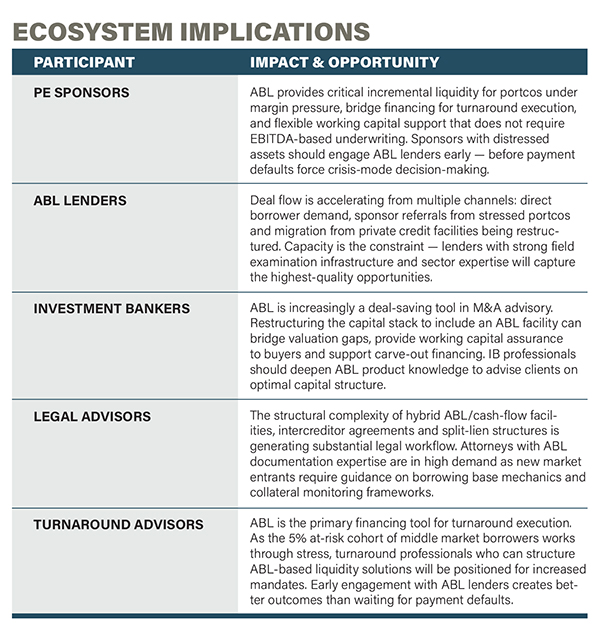

For most of the past decade, the asset-based lending market operated in the shadow of a private credit juggernaut that seemed to have all the answers. Cash-flow-based direct lending dominated the middle market’s financing conversation, fueled by abundant institutional capital and borrower appetite for covenant-light flexibility. But the first half of 2026 has delivered a sharp reversal of fortune — and ABL is emerging as the primary beneficiary.

The collision of private credit redemption pressure, rising default risk among leveraged middle market borrowers and tariff-driven economic uncertainty has created a moment of structural recalibration across the dealmaker ecosystem. For ABL professionals, the question is no longer whether the product will gain market share, but how quickly the market can absorb the demand — and whether the traditional ABL infrastructure is equipped to serve a dramatically broader audience.

The Structural Shift: From Shadow to Center Stage

The numbers tell the story of a product whose time has arrived. The global ABL opportunity is estimated at $32 trillion, dwarfing the approximately $9 trillion private credit market.1 Yet private credit managers hold less than 5% of that addressable market under management, reflecting years of institutional capital gravitating instead toward direct lending’s simpler corporate credit model.

That dynamic is now shifting. ABL has transitioned from a niche financing tool historically associated with distressed borrowers to a foundational element of the private credit landscape.2 Today’s ABL is being deployed proactively by public and private companies, as well as by private equity sponsors seeking incremental liquidity or more flexible capital solutions — even when cash-flow-based financing is technically available.

The industry conference circuit in early 2026 reflected this evolution. A major industry gathering dedicated an entire panel to the theme of ABL taking center stage in private credit, acknowledging billions of dollars in new private credit funds dedicated to asset-based strategies.3 While the investment methodology of many of these funds differs substantially from traditional asset-based lending, the capital flows are indicative of institutional investors’ appetite for collateral-protected returns in an increasingly uncertain credit environment.

Why ABL Now: The Convergence of Three Forces

1. Private Credit Stress Is Redirecting

Deal Flow

The most immediate catalyst for ABL’s ascendance is the stress unfolding across the private credit ecosystem. Investors have requested more than $10 billion in redemptions from private credit funds in Q1/26 alone, with Goldman Sachs projecting that fund assets could decline by $45 billion to $70 billion over the next two years if retail investors continue withdrawing.4 As cash-flow-based lenders face liquidity constraints and tighten standards, borrowers — particularly those with strong balance sheets but volatile income statements — are discovering that ABL provides a financing alternative that does not depend on the health of any single fund’s capital base.

One restructuring attorney captured the direction of travel: the market is returning to covenants, and private credit lenders are becoming more risk-averse in the aftermath of current disruption.5 That risk aversion is creating a direct pipeline of deal opportunities for ABL shops, as borrowers who might have secured 5x or 6x leverage from a direct lender 18 months ago now find those terms unavailable.

2. Credit Quality Divergence Favors Collateral-Based Approaches

KBRA’s surveillance of 2,416 unique middle market sponsored borrowers through 2025 reveals a market that is stable at the median but deteriorating at the margins.6 Multilevel downgrades increased 2.9 times quarter over quarter in Q4/25, with the rating agency attributing the uptick to sponsor and lender support becoming exhausted. When liquidity backstops are withdrawn, credit deterioration accelerates quickly.

The shadow default rate — measuring companies carrying distressed PIK or showing clear signs of economic stress despite technical covenant compliance — more than doubled from 2.5% in Q4/21 to 6.4% in Q4/25, according to Lincoln International’s index.7 For ABL lenders, this divergence between headline and actual credit health reinforces the structural advantage of collateral-based underwriting: when the borrower’s enterprise value narrative weakens, the tangible asset base provides a floor that cash-flow lending cannot replicate.

3. Regulatory and Market Dynamics Are Expanding the ABL Addressable Market

Post-pandemic working capital strain has not fully resolved and 2026’s tariff volatility is creating new pressures on inventory management, supply chain financing and receivable quality for middle market companies. Asset-based lending’s inherent flexibility — with availability expanding and contracting alongside the borrower’s collateral base — makes it structurally suited to environments where revenue predictability is challenged.

Clearing banks performed well in the ABL and invoice finance mid-market space through 2025, benefiting from competitive pricing and the ability to offer ABL alongside other banking products.8 Simultaneously, a wave of new fund-backed ABL lenders launched, recruiting well-known industry figures with demonstrated track records. These private credit entrants are bringing substantial capital to a market that has traditionally been capacity-constrained, potentially transforming the competitive landscape for 2026 and beyond.

The Blurring Definition: What Counts as ABL?

One of the most consequential developments is the expanding definition of “asset-based lending” itself. Traditional ABL — revolving credit facilities secured by accounts receivable, inventory, equipment and real estate — is well understood by middle market participants. But the new private credit ABL funds are financing a far broader range of assets: royalties, consumer finance receivables, aviation leases, NAV lending and other esoteric collateral classes.9

This definitional expansion creates both opportunity and complexity. For sophisticated dealmakers, the broadening asset class opens new financing structures — inventory monetization facilities, securitization-lite ABL transactions and hybrid cash-flow/asset-based products. For borrowers, it means more options but also more diligence requirements to understand the terms, pricing and structural implications of different ABL products.

The risk is that “ABL” becomes a marketing label rather than a meaningful underwriting discipline. Traditional ABL practitioners emphasize that the product’s value lies in deep collateral monitoring, regular field examinations and borrowing base mechanics that dynamically adjust availability — features that require specialized infrastructure and expertise. Private credit funds entering the ABL space with a cash-flow underwriting mentality and ABL branding may find that the operational demands of true asset-based lending exceed their institutional capabilities.

The Technology Edge: AI Meets Collateral Monitoring

A less-discussed but potentially transformative trend is the integration of AI and machine learning into ABL underwriting and portfolio monitoring. AI-enabled platforms can now ingest and analyze borrower data feeds continuously, identifying emerging trends — shifts in revenue mix, changes in customer concentration, working capital deterioration — weeks or months before they surface in formal financial reporting.10

For asset-based lenders, the integration of AI with real-time collateral monitoring through API connections to borrower accounting systems represents a meaningful evolution from the traditional field examination model. The competitive implications are significant: lenders that deploy these capabilities can underwrite more confidently, monitor more efficiently and intervene earlier when collateral trends deteriorate. The 47% increase in ABL professionals hired by private credit funds in recent years reflects a market that recognizes the human capital required to execute on these capabilities.10

Looking Ahead: What to Watch in H2/26

The ABL market enters the second half of 2026 positioned for a period of sustained growth, but several variables will shape the trajectory. The resolution of private credit redemption pressure will determine whether the current wave of borrower migration to ABL represents a structural shift or a cyclical blip. The pace of manufacturing sector stress — driven by tariff policy and supply chain disruption — will affect both the volume and quality of ABL collateral in industrial portfolios. And the competitive dynamics between traditional bank-led ABL shops and new private credit ABL entrants will define pricing, terms and market share for the next several years.

For the middle market dealmaker ecosystem, the message is clear: ABL is no longer a product of last resort. It is a first-choice capital solution for an expanding universe of borrowers, a growing institutional asset class and an increasingly critical component of the financing stack across the deal lifecycle. The professionals who position themselves at the intersection of these trends — with deep product expertise, strong lender relationships and the ability to structure creative solutions — will capture the greatest share of the opportunity ahead. •

Lisa H. Rafter is publisher of ABF Journal.