Managing Director

Huron Financial

Senior Director

Huron Financial

In 1965, Dr. Gordon Moore, a co-founder of what is now Intel Corporation, observed that the number of transistors found on an integrated circuit had doubled every year since its invention in 1958. Moore correctly predicted that this trend would continue indefinitely. “Moore’s Law” has proven true for not just the semiconductor industry, but for almost all modern computing technology — namely that change occurs rapidly and at an ever-increasing rate.

In February 2013, Standard & Poor’s included high technology industries among those at highest risk for credit ratings downgrade. An April 2013 report from market research firm IDC noted that personal computer shipments fell almost 14% year over year in the first quarter of 2013, due in large part to the popularity of smartphones and tablets as computing devices. This represents the worst decline in PC sales since IDC began keeping records in 1994.

These announcements highlight the risks of investing in the debt or equity of these types of companies; technological change and shifting customer preference can occur rapidly. Where enterprise value and cash-flows are based on intellectual property and new product innovation, valuations and the ability to service debt can swing wildly as innovation replaces older technology with new.

The value of intellectual property can be volatile. Therefore, organizational change in technology companies must occur rapidly. Time to change is compressed even more in companies with high fixed charges, such as debt service or capital requirements. Compounding the complexity of assessing technology companies’ valuations and cash-flows are byzantine revenue recognition rules, which can create a dramatic divergence between cash receipts and GAAP revenues.

The following presents a framework for situational analysis, turnaround strategies and tactics to address the financial challenges involving technology companies.

Situational Analysis

As with all turnarounds, a situational assessment is a critical first step to identify the root causes of distress and build a strategy to increase the probability of 1) short-term survival and 2) long-term viability. Unfortunately, in some situations neither short-term survival nor longer-term viability is possible. Determining this quickly can stem the flow of cash from the business and preserve its remaining value. In all situations, quickly and accurately identifying the barriers to success is the key to maximizing enterprise value for all constituencies.

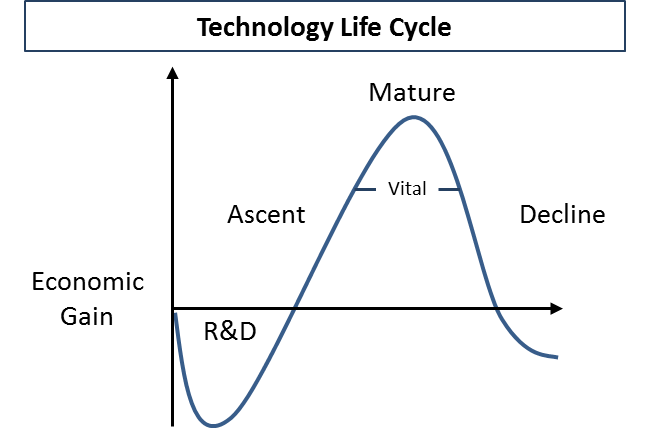

In technology turnarounds, identifying a product’s position in the technology lifecycle and assessing competitive threats should be the first stage of any situational assessment. Figure 1 illustrates the technology lifecycle. The array of potential strategic plans (longer-term goals, objectives and courses of action) is determined and limited by the technology lifecycle. For example, without additional investment in R&D, a product in the ascent stage may quickly become irrelevant. Conversely, increased investing in a declining technology may only make sense if the investment can extend the lifecycle.

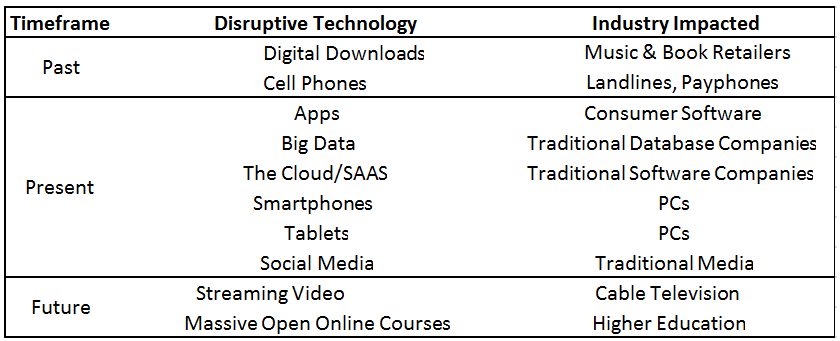

One of the challenges in dealing with technology companies is identifying the presence of disruptive innovation, which can dramatically accelerate the decline of a technology business. Some examples of past, current and potential future disruptive innovations are presented in Table 1.

An important second step in the situational assessment stage is to assess the product’s competitive position. This analysis facilitates additional refinement of the array of viable strategic alternatives in recognition of the competitive landscape.

The output of a situational analysis should be an outline of potential strategic plans and identification of the plan and tactics most likely to lead to success. Turnarounds are rarely linear; therefore, the strategy and tactics should be modified as needed as the turnaround progresses.

Technology Turnaround Strategies and Tactics

The situational analysis should provide strong guidance as to the appropriate strategy. The following are some effective turnaround strategies used with technology companies:

Niche Strategy — Focus on core products and customers and sell or eliminate non-core activities. This strategy will reduce operating expenses and increase management focus. It may be a viable strategy if one or more substantial segments will either remain as stable pockets of demand or will decay slowly.

Harvest Strategy — Maximize cash-flow over a relatively short term by:

• Avoiding any additional investment in the business,

• Greatly reducing operating expenses and

• Raising prices.

Leapfrog Strategy — Exiting the mature business through a sale, harvest strategy or wind down and placing all bets on products in the ascent phase of the technology lifecycle.

The list above is a partial list and often a combination of key elements can be used to craft the optimal strategy.

Setting a Plan

Once the strategy has been determined, setting out a plan to achieve it is essential. The plan should include the people involved, tactics and timelines. A wide variety of tactics are effective in technology companies; some of the most common are:

Evaluate product profitability — Contribution margin analysis by product and customer can be very beneficial. Identifying profitable and unprofitable products and customers supports an appropriate allocation of resources and may identify potential divestitures or pricing issues. It is important to model attrition rates to forecast future cash-flows, as inevitably customer preferences change over time. As with any turnaround situation, the company also must identify “core” versus “non-core” products. The outcome of this exercise may be to “fire” unprofitable customers, outsource manufacturing and/or maximize/optimize revenue streams. In the software industry in particular, high switching costs may provide an opportunity to increase pricing over the short term.

Divest non-core business lines — The sale of non-core assets can provide needed liquidity and sharpen management focus on aspects of the business critical to its future.

Rationalize headcount — Product profitability analysis often exposes opportunities to reduce development, sales and marketing, and support costs, recognizing that personnel costs drive innovation, and reductions can impact the future evolution of technology products and services.

Evaluate the sales approach — Often, companies adopt a direct sales strategy. Sometimes a partial or complete channel strategy can lead to cost savings. Importantly, a channel-driven approach may lead to a loss in control and revenue predictability.

Evaluate capital expenditures — Technology professionals like to work with the latest, “bleeding edge” technology. Identifying required technology tools, as opposed to desired, can create significant savings in infrastructure costs.

Evaluate the management team and incentives — Leadership during a turnaround is critical. Managers who are skilled and appropriate in a growth phase may not have experience or demeanor for managing financially distressed businesses and could benefit from experienced guidance or additional resources. Properly constructed incentive plans can motivate the sales force and management to “do the right thing.” Conversely, misaligned incentives should be identified and eliminated immediately.

Evaluate the capital structure and acquisition opportunities — Beyond operational improvements, debt restructuring (either out of court or through a bankruptcy) should be carefully considered. Often, companies or products in the decline phase of the lifecycle can benefit from synergies created through consolidation. An outright sale or combination of the business could be the optimal method to maximize the value of the enterprise for all constituencies.

Determining Useful Life

Perhaps the most difficult aspect of technology turnarounds is determining technology lifecycle position and the viability and remaining “useful life” of the products. These factors can dramatically change the strategic direction of the turnaround, whether to invest in growing and adapting the product to a changing market, or to cut costs associated with the products and “harvest” the cash-flows into their ultimate obsolescence.

The speed of change in technology organizations warrants quick and decisive action, and often advisors who are not emotionally invested in product development and rollout decisions can lend an objective perspective to the process of directing a technology turnaround. The tactics listed herein are certainly not an exhaustive list of the tools available, which must also take into account industry-specific considerations. Experience is vital to quickly assessing and acting on the various factors driving underperformance.

Ray Anderson, CTP, managing director, Huron Financial, specializes in leading companies through change. He has more than 20 years of senior operational and transactional experience as a corporate officer/board member, strategic advisor and investor in both growth and turnaround situations. He can be reached at [email protected] or 312-880-3172. Connect with Anderson on LinkedIn at linkedin.com/in/rayanderson or follow him on Twitter @andersonrc.

Stuart Walker, CIRA, senior director, Huron Financial, has more than 20 years of experience focusing on restructuring, finance, accounting and interim management matters. Walker can be reached at [email protected] or 214-365-2508. Connect with Walker on LinkedIn at linkedin.com/in/stuartwalker or follow him on Twitter @walkerstu.