Senior Managing Director

Focus Management Group

With 2020 nearly behind us, our attention can be directed to the future and how to deal with the long-term impacts of the ongoing COVID-19 pandemic on the U.S. economy. While the “new normal” has not been completely sorted out, asset-based lenders will be able to creatively use their existing tools to reduce risk going into 2021.

Accounts Receivable

Accounts receivable also must be analyzed for concentrations. It will be important to consider changes in customer concentrations to evaluate the need for additional or revised concentration limits. Customer bases may have changed, and concentration limits may need adjusting as well.

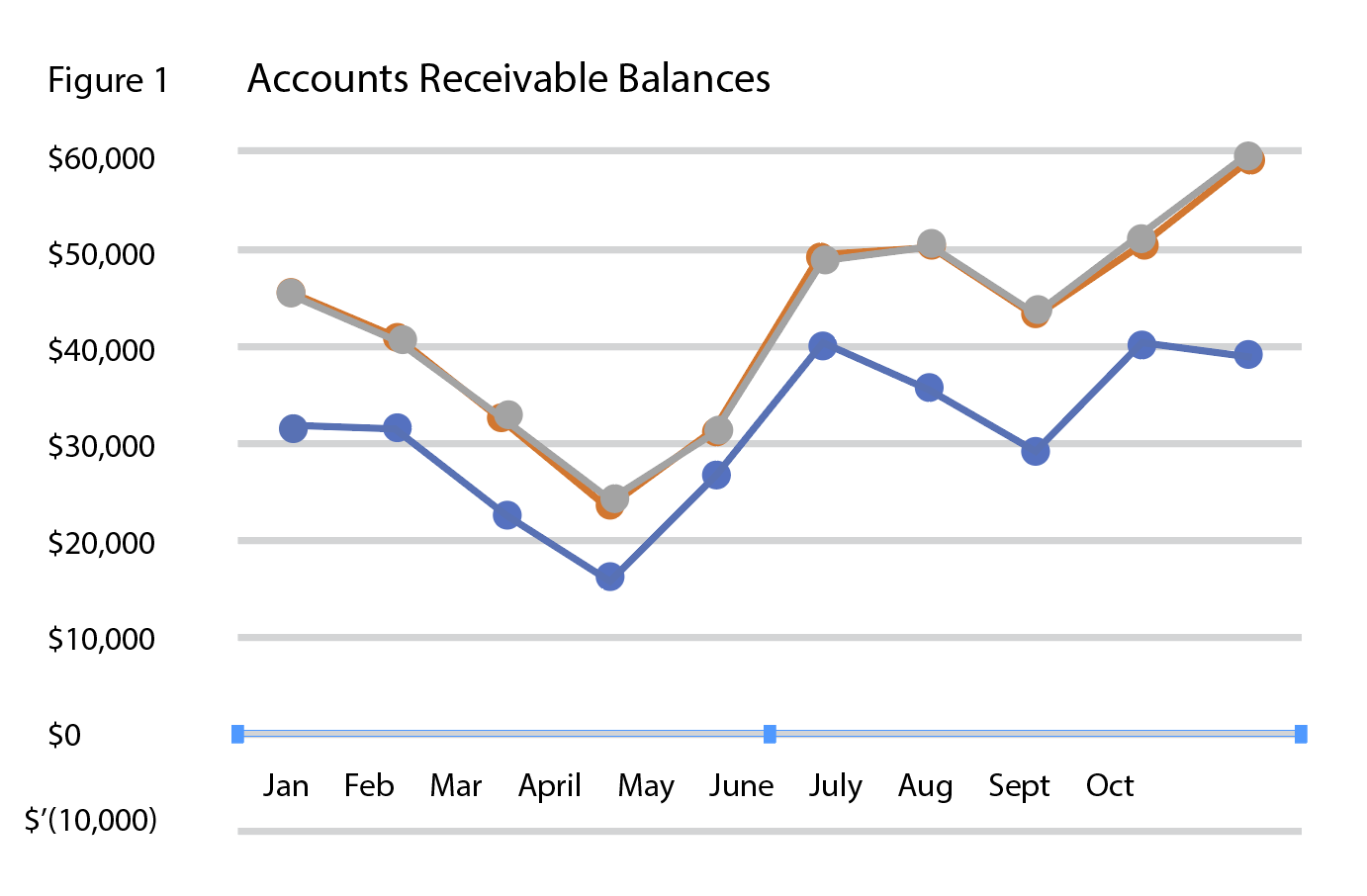

Figure 1 shows an example of accounts receivable balances from January to October of 2020 for a company that experienced an immediate reduction in receivables, then an increase in receivables, along with a delayed increase in past due balances.

Inventory

If the borrower provides customer purchase order, inventory and/or vendor purchase order relationships, lenders would be better able to assess the potential value of the inventory during a liquidation. Typically, a lender sees inventory turnover ratios by SKU; however, it would be even more beneficial to tie SKUs through the entire process. Expanding the scope of planned field exams to incorporate this analysis, or specifically requesting this information from appraisers, could enhance the decision-making around inventory advance rates and conversion to cash time periods.

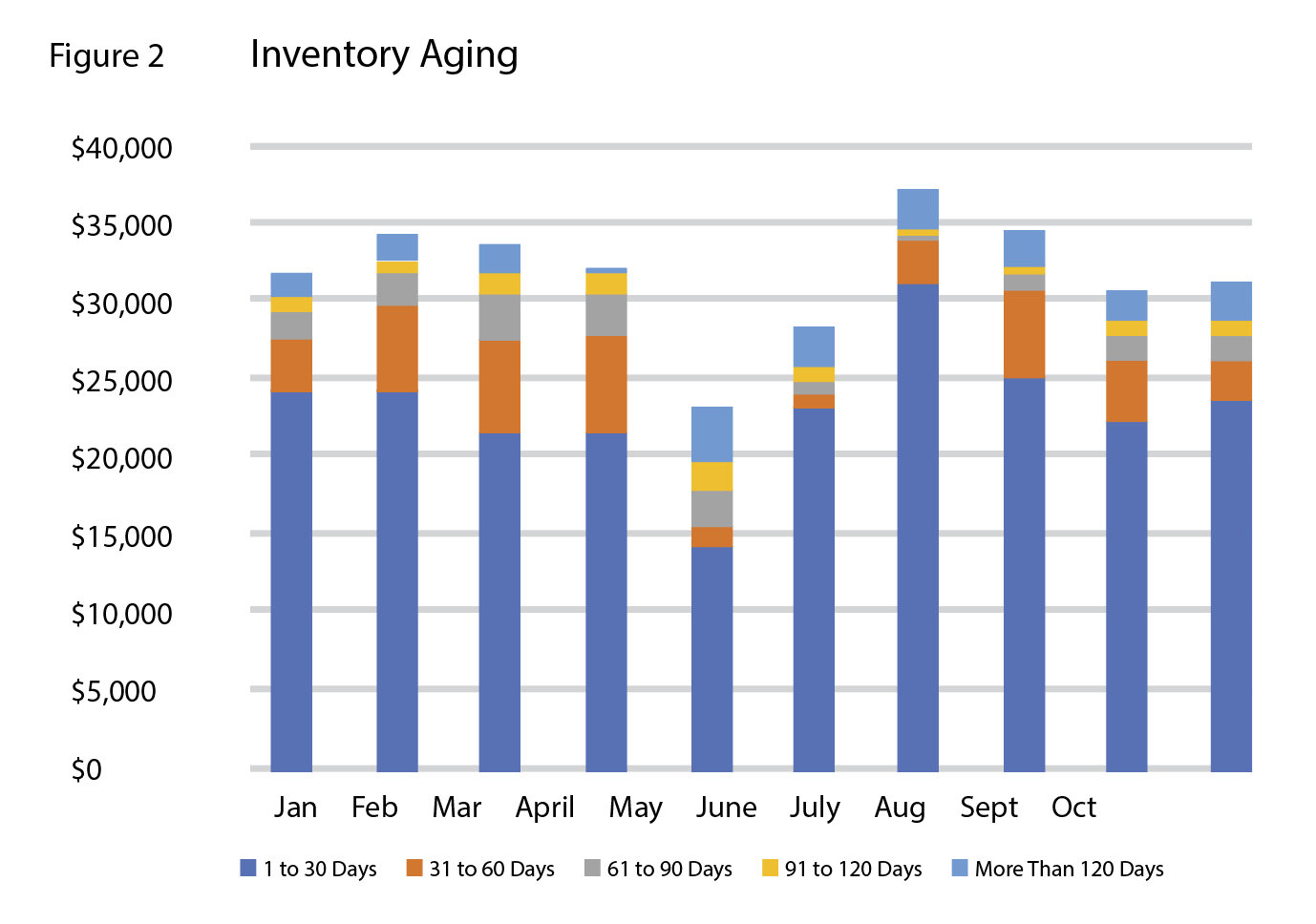

Figure 2 shows the inventory aging for the same company from Figure 1. After initial decreases in inventory levels, inventory increased, with the amount of current inventory showing the largest increases.

Relationship Between Accounts Receivable and Inventory

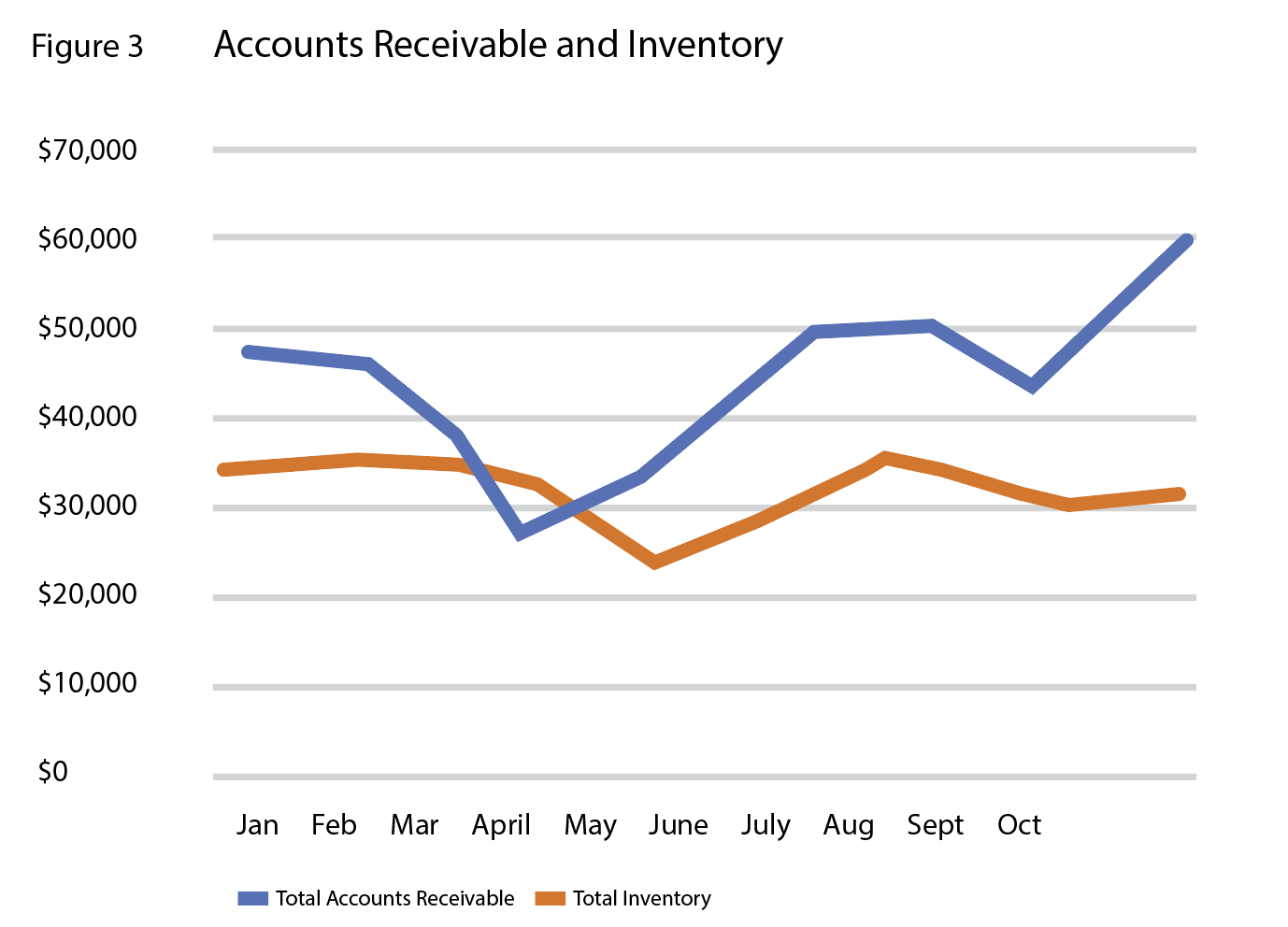

In Figure 3, the relationship between accounts receivable and inventory for the company from the previous figures shows a growing reliance on accounts receivable compared with inventory.

The required relationships between accounts receivable and inventory, and any caps on percentages, should be evaluated. The cap on the line of credit and the operating cycle also warrant additional discussion and review.

The receipt of 2020 performance information allows a lender to consider each borrower’s new normal. A lender should look at this time as an opportunity to underwrite a new line of credit or loan relationship. Because of the Q1 timing of COVID-19, borrowers should be able to provide three quarters, or nine months, of post initial COVID-19 impacts. The last few quarters of financial performance should be indicative of the new normal for most businesses.

With this information in hand, consider the revised operating cycle of the business. Calculate the operating cycle as of each month for the past year and evaluate whether the company has been asked to be a bank to its customers or its suppliers. Looking at the operating cycle will enable you to evaluate that aspect of cash use and discuss the operating cycle with the borrower.

2021 will continue to be challenging for lenders and borrowers. Reviewing accounts receivable and inventory information in conjunction with financial performance will help lenders restructure working capital lending. If lenders also evaluate accounts payable and accrued expenses, line of credit structures could be further enhanced. For example, if a business deferred the employer portion of payroll taxes, an ABL lender may want to determine the amount of that deferred liability and establish a reserve for the Dec. 31, 2021 and Dec. 31, 2022 payments. Lenders have elected to do everything from fully reserving the amount due in 2021 and 2022, to each year reserving a 12th of the annual payment as a monthly reserve building to the full annual amount due on Dec. 31, 2021 or 2022.

Use this opportunity to underwrite borrowers as new clients, gather detailed monthly information on all aspects of working capital, anticipate the operating cycle moving through 2021 and make sure the line of credit structure works for both parties. •

Juanita Schwartzkopf is senior managing director of Focus Management Group.

Schwartzkopf has more than 35 years of experience in commercial banking, business management and financial and management consulting. During her career, she has handled projects involving financing strategies, strategic planning, forecasting, cash management, creditor relationships, information management, bankruptcy, crisis management and business plan development.

Schwartzkopf has held key operating and management positions in many types of companies, from startup to mature businesses. Throughout her career, she has worked on improving performance in severely troubled and stable, healthy companies. She has negotiated lending arrangements on behalf of both creditors and debtors.