The leveraged credit market turned in another impressive quarter with high-yield bonds and bank loans gaining 5.7% and 3%, respectively. Ongoing accommodation from central banks across the globe has alleviated much of the initial macroeconomic tail risk posed by Brexit, but it may not be enough to dampen the seasonal volatility typically observed in the fourth quarter. Troubles in the banking sector, coupled with uncertainty surrounding upcoming political events — including the U.S. presidential election, the Italian constitutional referendum and key European elections — may weigh on risk assets for the balance of the year.

Among the looming dark clouds we also find silver linings. We estimate that Q3/16 U.S. gross domestic product growth will come in around 2.5%, supporting the view that U.S. economic growth remains resilient to global weakness. A rebound in oil prices also will help further fuel the recovery in the energy sector, and likely result in more spread compression. Looking further ahead, as the effects of a strong dollar and weak oil prices subside, we believe nonfinancial corporates are positioned to deliver strong performance in 2017, making any potential weakness in the fourth quarter a mere blip in the ongoing credit rally.

Q3/16 Leveraged Credit Performance Recap

The credit rally continued through the third quarter as high-yield bonds and bank loans delivered strong returns of 5.7% and 3.0%, respectively. High-yield bond spreads decreased 107 basis points over the quarter to 567 basis points. Bank loan discount margins decreased by 77 basis points to 505 basis points over the same period. High-yield corporate bond spreads remain 179 basis points wider than post-crisis tights, which suggests there is more room for spread compression, but prices temper our expectations. High-yield bond prices are averaging 94.9% of par, the highest since July 2014. Nearly all of the price upside exists in CCC-rated bonds, which are trading at an average price of 85% of par, whereas BB-rated and B-rated bonds are trading at 106% and 102% of par, respectively. On a sector basis, we believe the energy space continues to provide the greatest potential upside. Energy bonds, with average prices of 81% of par and yields ranging from 7.0% to 9.0%, look far more attractive than ex-energy bonds with average prices and yields of 101% of par and 5.9%.

Lower quality continues to outperform higher quality in both high-yield bond and bank loan markets. BB-rated bonds gained 4.3% for the quarter while B-rated and CCC-rated bonds gained 4.9% and 8.3%. BB-rated loans delivered a positive 2.1% return in the third quarter, versus a gain of 3.3% and 7.5% for B-rated loans and CCC-rated loans.

The bid for higher risk has continued with limited correction for longer than normal. In an effort to assess the historical context of current levels of volatility, our internal research found that the rolling 10-day VIX level has been higher than current levels 89% of the time since January 1, 2010. Prior to September’s brief spike in volatility, the 10-day average VIX was higher 98% of the time since 2010.

Inferring probabilities from past market behavior, we find it more likely that the VIX will rise than fall. It is important to note that we also typically see a pickup in volatility in October and November. Spikes in VIX are generally accompanied by declines in high-yield bond performance.

Fundamentally, we continue to believe it is too early to sound the alarm on high yield. The near-term outlook for high-yield bond defaults is improving as the upward trajectory in the 12-month trailing default rate slows. The 12-month trailing default rate ended the quarter at 4.85% on par-weighted basis, according to J.P. Morgan. Our view is that the high-yield default rate will decline over the next 12 months as the negative impact of declining metals and oil prices subsides. In loans, the 12-month trailing default rate of 1.95% remains well below the historical average.

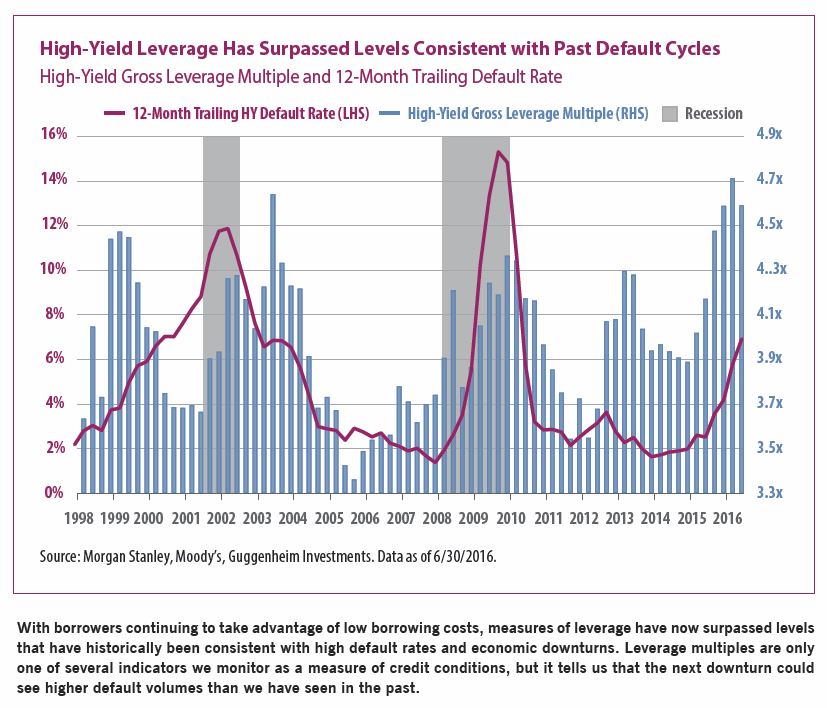

Rising Leverage Is a Warning Sign

Over the long term, our fundamental outlook for below investment-grade credit reflects a concerning trend in leverage: By either net or gross measures, the high-yield market leverage multiple has surpassed the historical peak, according to Morgan Stanley data. High-yield gross leverage multiples are currently averaging 4.6x compared to the historical average of 4x. The implication is that existing high-yield issuers who access capital markets will be marketing leverage multiples that make lenders fairly uncomfortable. We therefore continue to emphasize quality and stability of cash flows while avoiding sectors that are highly capital intensive. As the graph on the right illustrates, leverage is cyclically correlated to default rates.

Our concern has often been mitigated by relatively healthy interest coverage ratios, but these have also come under pressure as earnings weakened in 2015 and 2016. While the commodity sector can be blamed for the bulk of the deterioration, 2016 was also unforgiving to other sectors such as retail, which has been troubled by weaker-than-expected consumer spending. As of the end of the quarter, 19% of high-yield issuers in the retail space are trading below 80% of par, a level typically considered as distressed, signifying growing concerns over credit risk in this subsector. A recent Fitch report also highlighted seven retailers at risk of default, which appears to be reflected in the average price of outstanding bonds for those issuers. Mitigating these concerns, however, is the fact that interest coverage for ex-commodities issuers is not yet at levels associated with periods leading into an economic downturn, which tends to be at coverage below 3x earnings.

The fundamental picture for the bank loan market is much stronger. Earnings growth remains steady while interest coverage looks strong. Valuations in the loan market also appear stretched, however, with 44% of the secondary loan market currently trading above par. This is despite the fact that loans today carry only limited call protection (often in the form of a prepayment premium if the loan is called six to 12 months following the issuance date) or no call protection at all as the protection period has passed. At current levels, investing in secondary loans may result in a loss if the loan is trading higher than its call price. This increases the relative value of new-issue bank loans, which tend to price at discounts to par.

We saw plenty of opportunities in the primary market in September as new issue institutional loan volumes totaled $60 billion, a 176% increase over the January to August average of only $21 billion. Highyield bonds priced $28 billion in September, a 47% increase from the January to August average of $19 billion (although April and May 2016 volume exceeded September’s total). Increased volume has afforded us the opportunity to find attractive credits while remaining selective in the deals in which we participate.

High origination volume has been met by stronger demand from both loan mutual funds and robust activity in the collateralized loan obligation market, thereby strengthening the technical backdrop for loans. We expect both sources of demand will remain strong through the fourth quarter, allowing loan performance to remain steady. Through September, the loan market has delivered a stronger risk-adjusted return than most of the fixed-income market, including high-yield corporates, investment-grade corporates, Agency mortgage-backed securities, non-Agency CMBS, and even Treasurys. We believe the loan market currently looks more attractive than high-yield bonds as we go through the fourth quarter and look to reduce portfolio risk.