In 2011, Sherlock Holmes: A Game of Shadows and Downton Abbey were filmed at Waddesdon Manor near Oxford, England. Built in 1874, the Manor is a 100-room tribute to unparalleled luxury, in which Baron Ferdinand de Rothschild entertained clients and political allies. During the 1890s, Baron de Rothschild amassed a priceless collection of Renaissance art and gold snuff boxes which he kept in his new smoking room. His collection of exotic birds, kept in the aviary, was the envy of his contemporaries. One of the highlights of the baron’s collection is the extraordinary musical automaton elephant, dating from 1774, made by the renowned French clockmaker Henri Martinet.

The power and wealth of the Rothschilds was built on a combination of secured lending and what would be considered private equity investing today. The Rothschild’s banks were pioneers in providing secured financing of acquisitions ranging from the De Beers diamond mines in South Africa to the British government’s 1875 purchase of Egypt’s interest in the Suez Canal. In 1873, de Rothschild Frères in France and N. M. Rothschild & Sons of London joined with other investors to acquire the Spanish government’s money-losing Rio Tinto mines. Acting as both lender and investor, Rothschild turned the company around. The Rothschild bank also provided secured credit facilities to Cecil Rhodes in his development of the British South Africa Company.

European ABL Today

Fast forward to 2015. Asset-based lenders are financing the private equity sector across Europe, but the roles are much more clear-cut than in the early days of secured lending and private investment.

The focus of European ABL continues to be on the “beer-drinking nations” as opposed to the “wine-drinking nations.” In continental Europe, ABL is very focused on invoice financing, since enforcing inventory collateral is either untested in many jurisdictions or subject to local idiosyncrasy. (Explaining an inventory collateral enforcement problem in Barcelona to a credit committee sitting in Philadelphia could be dicey!) While it is possible to lend against inventory in France, many American lenders are cautious because of enforcement risk. Germany has recently enacted legislation to provide better visibility of inventory, which should clear the way for more transactions. But questions remain as to how inventory will collect out in Germany.

The promise of pan-European ABL spanning numerous countries and currencies has been muted by some of these issues. Many U.S. lenders do not hold banking licenses in some European countries, so participating in a pan-European ABL transaction such as ABN-Amro’s recent €180 million ($204.6 million) multi-currency ABL facility is challenging. The U.S. participants in this transaction were limited to the UK and Holland. A pan-European ABL opportunity in the market is now facing significant headwinds because the ultimate parent company is based in Italy and U.S. ABL players have difficulty getting comfortable with Italian judiciary risk.

Notwithstanding such doubts and queries that continue to surface around the use of SPV structures, there is evidence that ABLs are continuing to explore and exploit methods of funding receivables on a cross-border basis. As Andrew Knight, partner at Squire Patton Boggs in London, points out:

“The European market has accepted deals in which companies in certain European jurisdictions transfer their accounts receivable, once created, to a fellow group company — a trading company rather than an SPV, usually a company in England, but there have also been examples of companies in Ireland and the Netherlands being used for this purpose. The transferee company then takes the financing from the ABL and gives the transferred accounts receivable as collateral. Enforcements in the four or five cases that I know of in the past five years have been successful; without exception, the legal structure in each case has been proven to be robust and enforceable. It’s important to keep in mind, however, that the enforceability of these structures is dependent on certain operating rules being observed — they are pretty simple, basic rules but they do need to be followed. Personally, I prefer to bake them into the documentation rather than just trusting that the ABL’s ops team will remember to observe them.”

The Nordics represent a very attractive target for U.S. ABLs due to the region’s economic stability, favorable legal framework and transparency. However, pricing and terms for Nordic PE transactions reflect these attributes and the relative shallowness of the markets. The Mittelstand in Germany and Austria offers a deep pool of traditional ABL borrowers — manufacturers and distributors — and some U.S. ABL players are ramping up their efforts in this marketplace.

Uncertain Environment

As ABL players look beyond the UK and the Nordics, some are focusing on private equity sponsors as a way to mitigate some of the geographic risks. As a result, competition in the northern and western European PE marketplace is intense. One key reason is a growing imbalance of supply and demand.

According to Pitchbook and Merrill Datasite’s Q3/2015 PE Breakdown (see Exhibit 1), “By several metrics, private investment in Europe is sloping downward.” In Q1/2014, 1,381 European PE deals closed, compared with 880 in Q3/2015. “Europe’s PE market is maturing in an uncertain environment. One sign of maturation is the increase in bolt-on activity, which provides the advantage of allowing portfolio companies to expand geographically, no small task on a continent that speaks more than a dozen languages,” says PitchBook.

In London, the U.S. ABL player with the sharpest focus on financing middle market private equity firms is PNC. A typical transaction was the ABL revolver for Rutland Capital’s turnaround of Bernard Matthews, an agribusiness in Anglia. An important part of PNC’s private equity strategy is its ability to provide stretch financing through Steel City in the UK, which has a sweet spot of £10 to £20 million ($15.2 to $30.4 million).

A recent transaction that was square in the wheelhouse of Bank of America Business Capital in London was the £115 million ($175.1 million) credit senior secured facility to Hewden Stuart, used to refinance existing indebtedness, support working capital and CAPEX. Hewden Stuart is owned by an affiliate of Sun European Partners and is one of the UK’s largest plant and equipment rental companies. Hewden Stuart operates through a nationwide depot network and employs more than 900 staff, which gives rise to extensive day-to-day banking needs at the company. Treasury management is an attractive aspect of a transaction such as Hewden.

“ABL allows PE players to mine a rich vein of working capital to maximize debt capacity of the borrower,” says Jeremy Harrison, regional group head of Bank of America Merrill Lynch in London. “Because we can sharply define opening availability and collateral headroom in a transaction at a fairly early stage in the deal, we can provide the PE firm with good visibility to map out the pro forma capital structure.”

“Our goal is to find a long term flexible financing facility that maximizes liquidity and supports the anticipated growth of our portfolio companies,” says David Culpan, head of Debt Capital Markets — Europe at Sun European Partners in London. “We value early commitment to a transaction, as well as simplicity and flexibility.”

According to PitchBook, “As regulations tighten, median debt usage continues to remain low, despite the size of price tags (see Exhibit 2). That speaks to the level of scrutiny concerning leverage multiples PE firms and lenders remain under, with memories of the financial crisis still potent. It’s worth pointing out that equity proportions have been declining for several quarters now, due in part to sustained high prices. High valuations have persisted throughout the year, remaining a primary concern for buyers. Even if volatility in public markets has led to ripples of uncertainty and a decrease in public stocks, how much that will relieve private asset prices still remains to be seen. Already having dialed back activity by count in Q2/2015, general partners are wary of putting too much capital to work chasing inflated valuations.”

Wells Fargo Capital Finance is seeking to leverage its technology ABL expertise in the UK and select countries in Europe. Its model of lending against revenue streams from mission-critical technology is a proven winner in the U.S. and should gain momentum across the pond. Wells Fargo Bank is significantly increasing its focus on commercial real estate lending in the UK and Continental Europe.

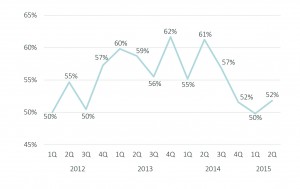

According to PitchBook, “At 52%, median debt usage in Q2/2015 marked the third consecutive quarter that debt levels stayed quite low, compared to 2013 and 2014. Regulatory scrutiny has helped keep leverage down, especially as banks have increasingly shied away from such risk. Even though alternative lenders such as BDCs are filling the gap and money remains cheap, PE investors are deploying debt cautiously.”

A legacy powerhouse in ABL and commercial finance, CIT is recovering lost market share in ABL in the U.S. now that its balance sheet has been repaired. Its recent merger with OneWest Bank promises to provide an additional measure of predictable and low cost funding. While CIT has not announced plans to re-open its London office, there is some talk in London’s Square Mile that CIT will resurface.

J.P. Morgan’s strategy is to focus on large transactions with its U.S. client base. J.P. Morgan has a small ABL team in London relative to the overall size of the bank.

Citibank is largely absent from leading any middle market ABL transactions in the UK and Continental Europe; its U.S. ABL teams are primarily focused on supporting its domestic corporate and commercial lending groups.

GE Capital’s asset-based platform in the UK, France and Germany is on the auction block at this point in time. Rumors in London are that the most logical buyer will be an Asian bank. In The Square Mile in London, the consensus is that GE Capital will be missed if no robust buyer surfaces. GE Capital’s innovation in structuring ABL transactions contributed to ABL’s prestige and appeal in PE circles. In Q1/2015, GE ranked second behind HSBC in the Europe Private Equity Deal League Tables, financing six PE transactions.

PE Exits on the Rise

The supply of ABL opportunities with European private equity sponsors is further constrained by the significant number of PE exits. According to PitchBook, “Soaring public markets have elevated public valuations, in turn boosting private asset prices substantially, making it easy for PE firms to primarily focus on the sell side (see Exhibit 3). Strategics are still competing for plum PE portfolio companies to keep growing as organic development remains anemic, which only further pushes prices upward. Q2/2015 saw a gargantuan $194 billion exited through 516 sales worldwide, pushing first half totals to $327 billion across 1,026 liquidity events. That figure puts 2015 on favorable footing compared to last year’s massive haul of $587 billion. In addition, the total capital exited in the Q2 was 16% higher than the previous high of the past four and a half years — $168 billion.”

Alternative lenders continue to proliferate in London, offering unitranche secured credit facilities across Europe. While some ABL players view alternative lenders as a threat, “the vast majority have limited appetite and in-house operational capabilities to finance working capital. Traditional ABL players can provide invoice and inventory financing on many of their bridging transactions,” says Piero Carbone, partner of Duane Morris in London. “Some of the leading U.S. alternative lenders in London include HIG Whitehorse, Fortress, KKR, Sankaty, GSO and AbleCo.”

However, some U.S. private equity sponsors use unitranche facilities provided by U.S. alternative lenders for European transactions, so the European ABL community never gets a look at the deal.

“Some ABL players will look to deliver every deal that a private equity sponsor is considering,” says David Culpan from Sun European Partners. “Depending on the specific transaction, the reality is quite different. The growth of debt funds providing unitranche has reduced the frequency that an ABL facility can compete against a cash flow based loan when looking to fund acquisition debt. That said, I believe there is a significant opportunity for ABL to compliment debt funds and compete against banks to deliver an alternative to the super senior revolvers needed in unitranche and high yield bond debt structures. This is extremely common in the U.S. and is an opportunity for growth in Europe.”

Knight agrees. “I believe the last two to three years will come to be seen as the period in which ABLs and PE each began to understand what made the other side tick,” he says. “We’re seeing much greater efforts on the part of leading ABLs to develop template documents that meet the specific needs of PE sponsors and funds alike, and a corresponding rise in the proportion of deals written with counterparties of that kind. Deal size and sophistication are increasing, with much greater attention being paid to debt-layering, split collateral inter-creditor issues and more co-operative exit strategies.”

The growing European chapters of the Commercial Finance Association and the Association for Corporate Growth are providing a forum for deal generation amongst the ABLs, PE firms and alternative lenders. “Our new CFA chapter is providing valuable education and awareness of the benefits of an ABL to the PE community,” says Harrison who is the CFA Europe Chapter president. “For example, in Paris this November, our chapter is hosting an event with two panels on various aspects of ABL. We expect a great turnout”.

“The ACG Eurogrowth Conference in mid-November will bring together PE firms across the continent with various secured lenders in a two day conference in Amsterdam. Important new relationships between PE sponsors and lenders will be formed, I am confident,” comments Piero Carbone, ACG board member and sponsor.

The Rothchilds navigated through booms, busts and devastating wars over three centuries, and emerged intact through the careful balancing of risk and reward. While fabulously wealthy, they never lost sight of the dangers of chasing a deal. The European economy still faces considerable volatility and headwinds with risks ranging from Chinese economic deceleration to the U.S. dollar’s strength to geopolitics. Today, private equity general partners are wary of putting too much capital to work chasing inflated valuations in Europe. The disciplines of ABL can provide PE firms with an excellent, objective sounding board to asset values and a valuable tool to smart investing.