Managing Director, Metals and Mining

B. Riley Advisory Services

Metals Market Recovery Analysis

Typical mill lead times have doubled and many metal service centers cannot restock fast enough. Machinery and equipment manufacturers as well as commercial truck and trailer manufacturers are seeing strong orders and increased backlogs. Overall, the steel market is currently buoyed by a release of pent-up demand as the economy recovers from the earlier restrictions of the COVID-19 pandemic coupled with limited supplies and higher raw material costs.

A similar V-shaped recovery is taking place for asset-based lending to metal service centers serving the automotive, appliance, machinery and equipment, transportation, infrastructure, and oil and gas industries. Appraisals of metal inventories such as steel, aluminum and copper are extremely time-sensitive, given the volatility of market prices, and this is especially true with the recent and sharp recovery in the metals market. Because of this, the effective date of an appraisal has a direct effect on borrowing base availability.

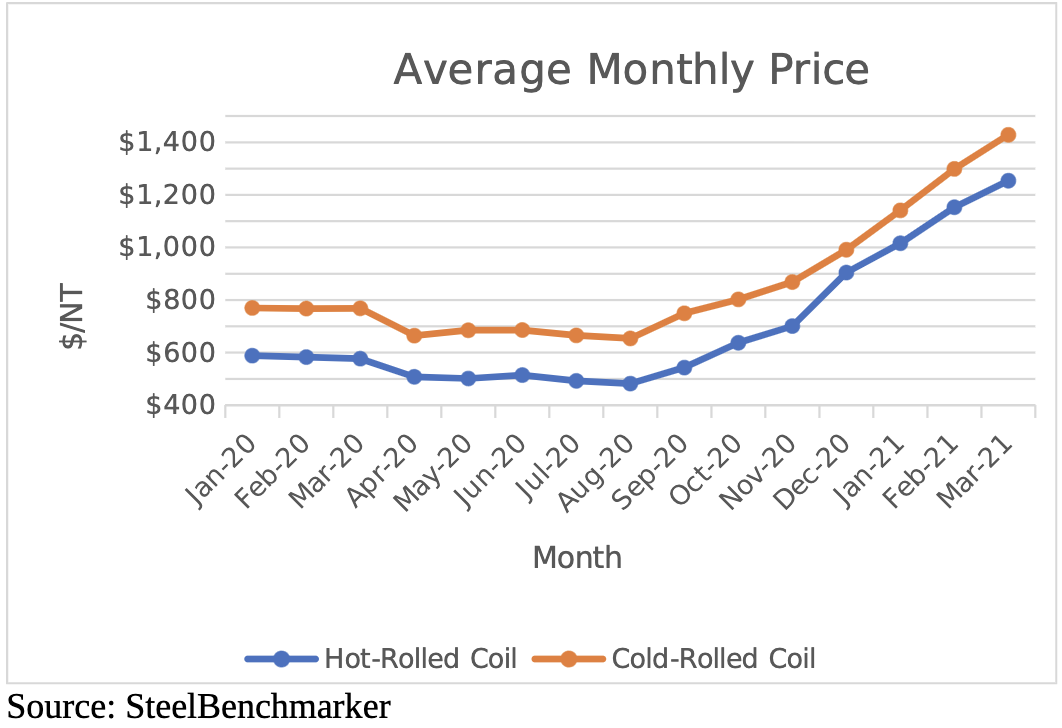

As a result of the impact of shutdowns and curtailments in the supply chain and manufacturing, North American automobile assembly operations were suspended in April and May of 2020, forcing numerous steel mills, though deemed essential businesses, to idle basic steelmaking. By May, carbon steel prices for hot-rolled coil fell 25% from mid-January 2020. In addition, raw steelmaking fell to 51% of total capability, a level not seen since 2009, versus 82.5% in late February 2020.

Many of our metal service center clients experienced sales declines of 25% to 30% in Q2/20. It took nearly four months, or until early September, for carbon steel market prices to show meaningful appreciation as manufacturing activity resumed.

Steel industry analysts and market participants are revising their forecasts on prices for flat-rolled carbon steel over the next three to six months, as market prices for hot-rolled coil, cold-rolled coil and galvanized steel continued to surge in February, March and April 2021 to historical highs. Domestic raw steelmaking capability continued to improve, reaching 78.7% for the week ending May 1, 2021, as steel mills strived to catch up to demand, according to the American Iron and Steel Institute. Yet lead times from both integrated mills and mini-mills are more than nine weeks versus the usual four to five weeks, with mill deliveries having the option to be late by up to three weeks.

Asset-based lenders and portfolio managers need to be attentive to the volatility in commodity prices as well as related factors such as mill lead times, metal scrap prices and the effects of tariffs on imports. This can only be done by a trusted appraisal and valuation services firm with qualified metals market knowledge, experience and market acceptance. As the effective date of a commodities asset appraisal can heavily influence a borrower’s inventory availability, a strong understanding of the market and appropriately timed appraisals are key to maximizing results. Frequent appraisals are valuable in keeping abreast of trends and avoiding surprises. •

Mike Petruski is a managing director with B. Riley Advisory Services (formerly known as Great American Group), a B. Riley Financial company. Petruski leads the firm’s metals and mining advisory services vertical in the valuations of ferrous and non-ferrous metal inventories, fabricated metals products, and machinery and equipment assets. With more than 30 years of industry specialization, Petruski has deep knowledge of international metals market pricing trends and works closely with asset-based lenders, investors and private equity groups on complex, syndicated ABL credit facilities and the valuations necessary to expedite such transactions. He is a member of the Secured Finance Network and the Turnaround Management Association. He can be reached at mpetruski@brileyfin.com.