Partner

Husch Blackwell

Partner

Husch Blackwell

A strange confluence of geopolitical events, labor unrest, softening consumer demand and supply-chain logistical issues could leave lumps of coal in the stockings of lenders this holiday season.

The story begins in the Red Sea, where attacks on international shipping by Houthi rebels have forced ocean carriers to divert ships around the Cape of Good Hope in South Africa, adding significant time and cost to the journey. The attacks began in October 2023 as a form of reprisal for Israel’s invasion of the Gaza Strip and have varied week by week in number and intensity; however, the cumulative effect is that large container ships are routinely diverted, creating dislocations across the global supply chain.

Such diversions are thought to be the proximate cause for the rapid run-up in shipping rates throughout 2024, causing many logistics professionals to experience flashbacks to the COVID-19 pandemic. Despite the spike in rates, they are just a fraction of what we saw during the pandemic. Still, rates are up over fourfold in some instances since the beginning of the year, and while many experts see the current inflation in rates as something greater capacity can cure, it is unclear when and to what degree such capacity can be deployed. Meanwhile, rates could still be trending upwards; the Freightos Baltic Index surpassed $5,000 in mid-July for the first time since September 2022.

Against this backdrop, a far more destabilizing event looms on the horizon. On June 10, the International Longshoremen’s Association (ILA) issued a press release announcing its refusal to continue negotiations due to an outstanding dispute with a terminal operator involving one Gulf Coast port. The ILA has signaled its willingness to call for a coastwide strike if a new contract agreement is not reached prior to the expiration of the current contract, which covers roughly 45,000 dockworkers at seaports on the U.S. East and Gulf Coasts. The current contract expires on Sept. 30, 2024.

A coastwide strike kicking off the fourth quarter would create significant challenges for shippers. The freight rate inflation and the potential for a massive work stoppage have led many shippers to pull forward overseas orders. According to Freightos, a transportation services and information firm, peak season shipping volumes are “earlier than usual in the year” as a result of “efforts to account for longer lead times due to Red Sea diversions and avoid delays later in the year and closer to the holidays, bring in shipments before possible labor disruptions at U.S. East Coast ports, and beat some new tariff roll outs in July and August.”

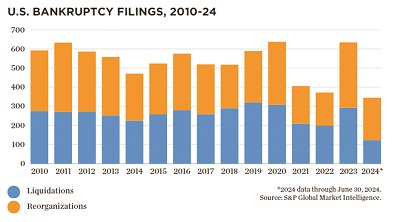

This pull-forward is forcing companies to make longer-range inventory and sales projections for the holiday season. For consumer-adjacent businesses, like retail, this can be a risky practice, especially as recent data suggest a softening of consumer demand in the U.S. If this earlier-than-usual inventory build miscalculates holiday demand, the results could be severe, especially for enterprises that are already struggling with financial distress, which are growing in number. In 2023, corporate bankruptcies reached levels not seen since 2011, and the first half of 2024 is trending above last year’s level.

THE LUXURY OF TIME

Lenders to consumer-adjacent businesses should use this time to assess what kinds of additional risk the circumstances outlined above present for their loan books. The worst time for a lender to learn that it has a defect in its loan documents is when its borrower is facing financial difficulties. Savvy borrowers will try to leverage key defects to get big concessions from the lender. The better approach

is to cure those defects before the borrower is facing hard financial difficulties. The lender must carefully review the underlying loan documents to make sure there aren’t any defects. This includes ensuring all loans were properly documented, that lien descriptions are accurate and that corresponding Uniform Commercial Code (UCC) and real estate related filings provide the lender with a properly

perfected status.

Aside from making sure the lender is properly perfected, lenders also must check the respective pecking order of other secured creditors. In retail industry scenarios it is very common for certain lenders to do inventory financing. The rules for properly perfecting inventory financing are different than other run-of-the-mill security arrangements. Inventory lenders must give notice of their liens prior to the borrower taking possession of the inventory. Relatedly, companies in financial difficulties will frequently turn to factoring arrangements as a means of generating quick cash.

When assessing credit risk, it is also very helpful to understand what a borrower’s capital structure looks like. Prior to a borrower entering distress, creditors should take the time to “war game” an insolvency event. What will your borrower do? What will the other creditors likely do? What can you do now to better position and strengthen yourself in the event of a future insolvency situation?

GRADUALLY, THEN SUDDENLY

When asked how he went bankrupt, a character in Ernest Hemingway’s The Sun Also Rises replied, “Two ways. Gradually and then suddenly.” Assessing risk cannot be a one-time, static exercise, because the nature of risk changes, and during crisis events, the changes can be rather sudden. It is extremely important to monitor the health of your borrowers, to write provisions into agreements

that mandate reporting, and to devote the resources needed to decipher inbound data. Doing so should throw sunlight on what is often a blind spot for lenders: the current state of the borrower’s financial situation. Failure to get visibility into current financial information will hamper efforts to protect the creditor’s position and, potentially, allow the borrower to service unsecured creditors ahead of the secured lender.

When a borrower has consolidated its cash operations and borrowing with one bank, the lender’s ability to monitor day-to-day cash flow is obviously much enhanced. Likewise, when a borrower seeks to move its accounts to another institution, that should be a red flag that requires extra diligence.

Ultimately, poor financial reporting can be the source of a default under a well-written loan agreement. The lender needs to signal that accurate and timely financial reporting is essential and the lender won’t hesitate to call a default if the borrower doesn’t strictly adhere to its reporting requirements.

IT’S ONLY MAKE-BELIEVE

A common error that lenders make is letting a borrower overextend its line of credit (LOC). It’s an easy mistake for lenders to make; banking is a relationship business, and nothing signals trust and steadfastness quite like bankrolling a customer through a tough stretch. A more disinterested view of the data, however, suggests that LOC overextensions usually resemble the “extend and pretend”

practices found in commercial real estate (CRE) lending.

Unlike CRE, where loans potentially unwind over a period of years, consumer-adjacent businesses, like retailing, have a much shorter runway for distress. Enterprise-threatening events erupt and resolve in a matter of months if not weeks.

We won’t suggest that these are easy decisions for lenders to make. Sometimes, though, it is easier to make decisions by widening your lens. After all, if one loan sours, it’s usually just the borrower’s

problem; however, if an entire portfolio goes under, then it becomes the bank’s problem. If a lender has high exposure to similarly situated borrowers, it may have to be more aggressive, even if in the normal course of events it might be inclined to extend the borrower. In any event, lenders need to ensure that they at least have options available, and that can only happen if the underlying agreements allow the necessary diligence to take place.

COLLATERAL, COVENANTS & GUARANTIES

Beyond the financial condition of the borrower and putting into place the monitoring needed to make key decisions, lenders should revisit and test the assumptions that underlie the collateral, covenants and guaranties in their loan agreements. For instance, a lien in accounts receivable has been described as a glorified unsecured creditor. In a similar manner, then, a lien in retail inventory is not worth much if the business goes into liquidation mode. It is critical to properly and realistically value collateral so that proper loan-to-value ratios can be determined. This also means pushing back on appraisals,

if they are available. If an appraisal seems overly optimistic at first blush, then it probably is. Collateral valuations should also consider insurance and whether the lender is named as a loss payee and that the policies are in good stead.

Lenders should always and forever signal to borrowers that loan covenants are taken very seriously. This can be done in word and in deed. Obviously, lenders can remind borrowers of this through constant messaging to this effect, but conduct is also important. For example, establishing an early-warning system for borrowers when they get close to covenant violations is a non-threatening and useful way to reinforce the message. It can also be helpful to good-faith borrowers who can take corrective action to avoid a default.

Guaranties also deserve scrutiny when credit risk rises. Like loan documents, guaranties need to be properly documented and free of defects. It is also helpful to understand whether guarantors can pledge additional collateral if needed and whether guarantors are themselves experiencing distress that could impact the pledge.

DO WHAT IS NECESSARY, BUT NOTHING MORE

Once any available fixes are exhausted, both borrower and lender are left with options that range from bad to worse, so it is important to see things for what they are. If default is where things are going, sometimes it best to get there early. Forbearance agreements can be extremely helpful because they greatly sharpen the borrower’s focus, spell out very clear benchmarks that a borrower must meet and

result in releases of lender liability claims.

But lenders should avoid overreaching with a forbearance agreement. Some lenders see forbearance agreements as a revenue source or an opportunity to generate more fees. They certainly can do so, especially in the short run, but it is a business approach built on melting ice cubes. It is far better to craft realistic forbearance agreements that create the conditions for a win win situation. Avoid punitive provisions that throw up complications with no real long-term utility.

This is especially apt for the potential scenario described at the outset. Businesses stumble into distress for many reasons, but when the culprit is a combination of exogenous macroeconomic factors, there is a decent chance that an enterprise can survive with a little good luck — and a lender that understands how and when to apply the proper remedy. •

Michael Fielding is a Kansas City-based partner with Husch Blackwell and a member of the firm’s Insolvency & Commercial Bankruptcy team.

Brent Salmons is a partner with Husch Blackwell’s Washington office where he focuses on corporate transactions involving highly regulated industries, like cannabis and renewable energy.