No Late Rescue for Loan Volume

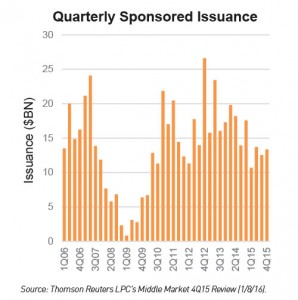

In 2015, sponsored middle market loan volume reached $50.3 billion, down 28% from 2014, falling below expectations and capping the weakest year for volume since 2009 (See Figure 1). Issuance dropped every quarter year-over-year, and 4Q15 was no exception. Despite volume rising 7% from the third quarter, at $13.4 billion, fourth quarter volume was still down nearly 25% from the prior year period.

For many lenders, including Fifth Street, the typical seasonal push that occurs at calendar year end was muted in 20151. A number of factors contributed to the protracted slowdown in sponsored deals, including an increase in borrowing costs and buyer/seller divergence stemming from lower deal quality and lofty valuations, as strategic buyers continued to drive up multiples. Combined, these factors have created a more challenging environment for sponsors, many of whom we believe have chosen to wait on the sidelines in hopes of better returns.

Vintage Years on Tap

While many lenders expect volumes to be flat in 2016(2), we hold a more hopeful view for middle market sponsored lending. With backlog down from recent years, we are not expecting a rebound in the first quarter, but believe things should pick up later in 2016, as the market gradually adjusts to the new reality of higher borrowing costs.

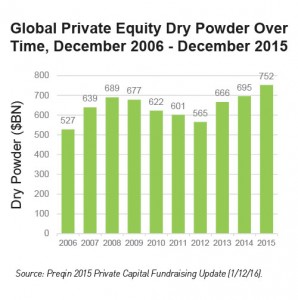

Private equity firms have raised considerable capital and have record amounts of dry powder at their disposal. The level of unspent capital reached a record of $752 billion by the end of 2015, up from $695 billion the prior year, which will need to be put to work at some point (See Figure 2).

We believe that years from now, lenders with capital to invest in new loans will look back on the vintages of 2016 and 2017 as similar to the favorable vintages of 2009 and 2010. With spreads widening, it seems that prudent lenders will start getting adequately paid for risk. Given crashing oil prices and the disarray in high-yield, we think the table is set—as it was in the aftermath of the financial crisis of 2008—for lenders to deploy capital into deals with strong risk-adjusted returns. It could be an exciting opportunity for lenders with long-term capital and the flexibility to selectively deploy it. However, absent discerning underwriting, capital is not enough. Instead, a high level of selectivity driven by superior sourcing represents the key to success in our view.

Yields Widen, Hurting Dividend Recapitalizations

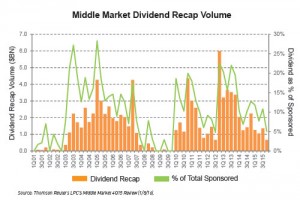

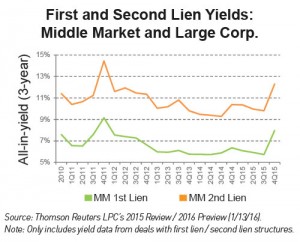

For the first time in a few years, yields are significantly higher in the middle market. Assuming a three-year duration, the average yield for a middle market first-lien term loan is at the highest level since 2012, climbing to 7.14% for the quarter, up from 6.25% in 3Q15 and 5.96% in 2Q15(3). Notably, higher yields have created significant headwinds for dividend recapitalizations, which had volume of just $4.3 billion for all of 2015, representing a 38% decline from 2014 and the lowest level in six years (See Figure 3).

Banks: Enforcement Breeds Uncertainty

The ongoing shift in market share towards nonbank lenders continues to change the complexion of the middle market. While the leveraged lending guidelines have been finalized for some time, banks are currently wrestling with enforcement. The OCC (The Office of the Comptroller of the Currency) appears to be taking a very strict approach—with some arguing that lending criterion has become a moving target.

Facing uncertainty over what may or may not get approved, banks appear hamstrung in terms of where they can participate right now. However, when they finally encounter a transaction that falls squarely into their box and seems to be within the regulatory parameters, expect them to pursue the business very aggressively.

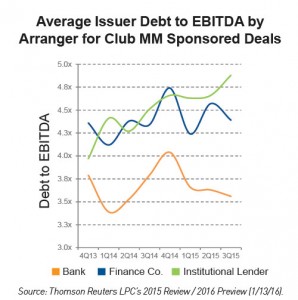

In short, we believe we are likely to see a continued pull-back from banks given ongoing regulatory pressures—a trend that should continue to benefit alternative lenders (See Figure 4).

Flight to Quality Impacts Second Lien

Amidst weaker volume, there still appears to be ample capacity in the middle market. However, lenders continue to gravitate to certain credits over others, with many focused on plain vanilla companies with no noise and minimal adjustments. Additionally, in a noticeable flight to quality, many lenders continue to migrate to senior, floating rate securities2. This is not unexpected, as periods of volatility tend to create a risk-off response and a move up the capital structure.

To that end, middle market second lien volume reached just $2.5 billion for the year—a 64% decline from 20143. The diminished appetite for second lien volume can also be traced to a weakened buyer base: many BDCs are currently trading below book value, while hedge funds have had to reassess and redeploy their own assets in the wake of a tumultuous 2015. The heightened uncertainty has unsettled sponsors, many of whom are proceeding straight to the unitranche product given the certainty of close, versus a first and second lien structure4.

Given the sharp drop-off in second lien bids, yields on middle market second-liens moved drastically wider this quarter. The average yield has risen to 12.31%, up 249bps from 9.82% in 3Q15 (See Figure 5). The resulting supply/demand imbalance leads us to believe that selective opportunities for strong-risk adjusted returns in second lien may lie ahead.

Markets Shrug Off the Fed

The Fed’s recent interest-rate hike was both widely anticipated and priced-in by market participants and, in our view, has had a de minimis impact on the middle market.

Amid weak economic indicators, we expect the Fed to proceed slowly and cautiously with future increases. Since uncertainty remains in the markets, we believe policymakers will try to avoid adding to it with interest rate surprises. For that reason, the middle market should be able to absorb future increases without undue stress.

Anticipating a slow rise in interest rates, Fifth Street has continued to position itself to take advantage of an up rate environment, seeking to blend down the level of LIBOR floors in its deal structures. Generally speaking, lenders don’t generate additional income and benefit from a rising interest rate environment until LIBOR surpasses the LIBOR floor, which had typically been structured at 100 basis points in recent years. By beginning to complete new deals with lower or no LIBOR floors, lenders are beginning to focus more on capturing spread and benefitting earlier from the rise in rates.

Recently, Fifth Street led its first deal in some time with no LIBOR floor and in the coming months, we expect to see LIBOR floors under pressure.

Where Will Middle Market Lending Go in 2016?

Regardless of the pace of future rate hikes, we believe that the cost of capital is unlikely to go down. However, if the economy remains stable and we do not see a drastic increase in supply, we would expect purchase price multiples to stabilize over the next several quarters.

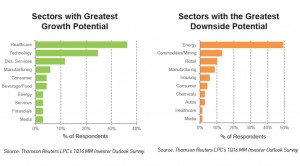

While no one can predict where credit quality will go, we are anticipating patchy growth and sector divergence. For instance, as we have noted for some time, we see ongoing strength in healthcare and technology. On the other hand, we continue to maintain that energy has further downside potential and has not yet reached its inflection point (See Figure 6).

We believe it is prudent to avoid the cyclical industries while taking a more cautious approach to the higher valuation/higher leverage industries that generate high free cash flows. Conversely, we also counsel a shift toward safer, more recession-resistant sectors. Deals in the former category are still getting done; however, that universe seems to be waning today.

Middle Market Direct Lending continues to gain increased attention as an asset class, with many investors particularly attracted to the yield and relative protection that senior secured and unitranche loans can provide.

Due to Fifth Street’s 17-year track record of creating value through proprietary origination capabilities, discerning underwriting and portfolio management expertise, a variety of stakeholders have been looking to access our award-winning direct origination platform from a number of angles.

A Record $3 Billion in Agented and Syndicated Loans in 2015

As we have continued to expand our capital markets presence over the last few years, the volume of our middle market syndications and club transactions has risen, which is partially attributable to increased interest from third parties to participate in our deals. These participations allow third parties, often lenders who do not have origination platforms of their own, to access loans that have not only been selected through our rigorous investment process, but are also supported by our established top-tier sponsor partnerships.

Fifth Street set a new company record last year, with over $3 billion of deals agented and syndicated in 22 deals across our platform5. This represents a 67% increase over the $1.8 billion of deals agented and syndicated in 2014.

Separately Managed Account Closing

In further testament to the strength and value of the Fifth Street platform, earlier this month, we announced the closing of a Separately Managed Account (“SMA”) with a large, well-respected institutional investor who intends to purchase $50 million of middle market loans in the SMA.

Our platform’s ability to provide customized solutions across the capital structure to middle market companies and gain access to exclusive opportunities makes an SMA a compelling product for institutions seeking middle market asset exposure. Recent interest from institutional investors also led to Fifth Street’s closing of two collateralized loan obligations (CLOs) in 2015, as well as joint ventures with each of our business development companies (BDCs) in 2014.

We are looking forward to beginning our relationship with our new client and remain excited about the prospects of growing our institutional business line.

Footnotes

- Brown Gibbons Lang Annual State of the Middle Market (December 2015).

- Thomson Reuters LPC’s 1Q16 MM Investor Outlook Survey (1/4/16).

- Thomson Reuters LPC’s 2015 Review / 2016 Preview (1/13/16).

- Thomson Reuters LPC’s Gold Sheets Middle Market (December 2015).

- According to Thomson Reuters LPC League Tables.