Private equity is sitting on the largest inventory of unrealized portfolio companies in the industry’s history, and the pressure to move is intensifying from every direction — limited partners demanding distributions, fund lifecycles approaching their natural endpoints and a competitive landscape where the firms that return capital fastest will raise the next fund most easily. The question that has defined PE for the past three years — when will the exit logjam break? — is finally resolving, but the answer looks different from what most participants expected.

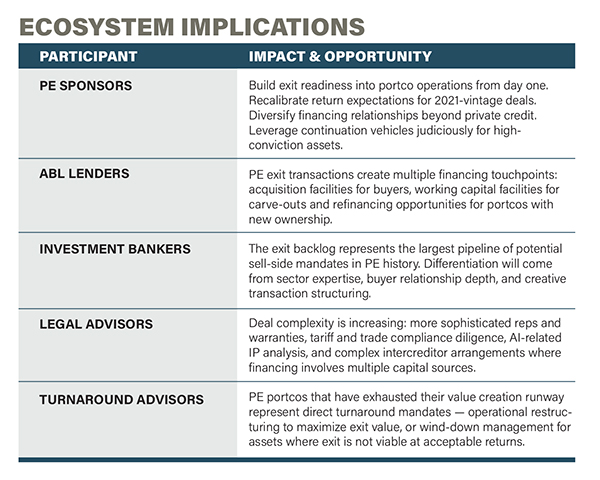

For the middle market dealmaker ecosystem, the PE exit backlog represents both the largest near-term opportunity for transaction volume and the greatest test of collaborative problem-solving across the financing stack.

The Scale of the Backlog

By the end of 2025, the global inventory of PE-backed companies rose to approximately 32,500 — up from 29,400 a year earlier — with a growing share held beyond targeted holding periods.1 In the middle market specifically, the median holding period has stretched to 5.8 years, and data shows more than 6,600 companies held between five and seven years, representing prime candidates for near-term exits.2

PE firms that acquired companies in 2020 and 2021 at peak valuations, often with aggressive leverage, are now five years into hold periods with limited runway to generate expected returns.3 In the first half of 2025, U.S. PE deal value rose roughly 8%, putting a dent in available capital — dry powder held by U.S.-based PE funds dropped to about $880 billion from a record $1.3 trillion.4

WHY THE LOGJAM IS BEGINNING TO BREAK

Financing Conditions Are Easing — Selectively

The average cost of funding for a PE middle-market term loan has fallen by approximately three percentage points from the prior peak, with scope for further reduction.5 This easing is narrowing the valuation gap that has frozen many transactions.

Middle market deal activity has started 2026 with genuine momentum. M&A advisors report that deals in the pipeline are priced at more realistic levels, the buyer-seller expectation gap has narrowed and pre-COVID diligence rigor has returned.6

Strategic Buyers Are Intensifying Competition

According to BDO’s PE survey, 43% of fund managers report that most deal competition will come from strategic buyers, whose ability to pay higher prices is creating both buy-side challenges and more favorable exit conditions for sponsors.3

Creative Exit Mechanisms Are Multiplying

Secondary transactions have become an increasingly important relief valve. GP-led continuation vehicles and other secondary structures are providing liquidity where traditional exit routes remain constrained.1 These structures are increasingly used not just to manage timing risk but also to support longer value-creation horizons for assets requiring sustained investment or operational transformation.

The Private Credit Complication

Just as the PE exit environment is improving, stress in private credit is constraining the availability of acquisition financing. Spiking redemptions in private credit create short-term hurdles for M&A.7 Sponsors are diversifying beyond direct lending to include ABL facilities, broadly syndicated loan markets and traditional bank financing in their capital structure plans.

Distressed Exits: The Growing Opportunity

With significant PE dry powder still available, 2026 is expected to be an aggressive year for middle market M&A in distressed situations — especially carve-outs and strategic asset sales. Distressed middle market businesses may attract opportunistic buyers seeking operational upside.8

AI as a Valuation Driver and Disruptor

AI is no longer a thematic overlay — it is a valuation-defining variable. FTI Consulting reports that 65% of PE respondents marked AI as a top priority in 2025, and AI is now embedded across the PE lifecycle.4 Morgan Stanley notes that more than half of its middle market portcos have active AI initiatives.5

For exits, AI readiness is becoming a differentiation factor. Portcos that demonstrate measurable AI-driven productivity gains will command premium multiples. Non-differentiated PE platforms that lack depth to deploy AI resources effectively will end up on the short end of the K-shaped recovery.5

The H2/26 Outlook: Cautious Momentum

The ingredients for meaningful acceleration in middle-market PE exit activity are largely in place. PwC’s assessment captures the trajectory: outperformance will be driven by operational improvement, sector specialization and data-enabled transformation — not financial engineering.9

For the middle market ecosystem, the message is one of prepared optimism. The deals will come. The question is whether each participant — sponsor, lender, banker, attorney, turnaround professional — is positioned with the right capabilities, relationships and market intelligence to capture their share of the recovery. •

1 Global M&A Trends in Private Equity: 2026 Outlook, PwC Global, Jan. 27, 2026.

2 Ravikumar, Divya, “Thousands of Portfolio Companies Are Ripe for Exit,” Private Equity Info, May 27, 2025.

3 “2026 Private Equity Industry Predictions, BDO, Jan. 9, 2026.

4 “Four Predictions for Private Equity in 2026,” FTI Consulting, February 2026.

5 “Alts In Focus: 2026 Private Equity Outlook,” Morgan Stanley, April 6, 2026.

6 Connolly, Robert, “Outlook for Middle Market M&A and Private Equity 2026,” LP Legal, “Feb. 4, 2026.

7 Tully, Shawn, “The $265 Billion Private Credit Meltdown,” Fortune, March 2026.

8 “Distress Makes a Comeback,” Capstone Partners, Jan. 6, 2026.

9 Private Equity: US Deals 2026 Outlook, PwC US, 2026.

Lisa H. Rafter is publisher of ABF Journal.