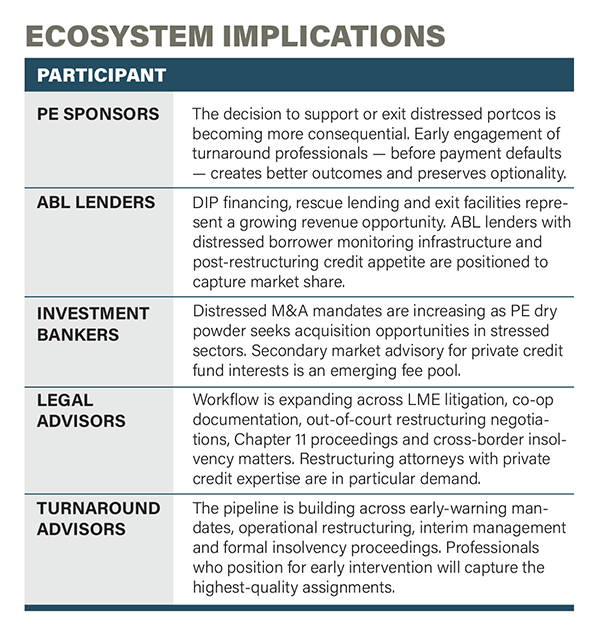

For turnaround advisors and restructuring attorneys, 2026 is not the year of the tsunami. It is something potentially more lucrative and more sustainable: the year of the rising tide. The middle market distress cycle built through 2025 continues to accelerate along multiple fronts — credit quality deterioration, maturity wall pressure, tariff-driven margin compression and private credit fund stress — creating a restructuring pipeline that industry veterans describe as the most robust in years.

But the nature of the work is evolving. The traditional Chapter 11 filing is no longer the default tool; liability management exercises, out-of-court restructurings and creative capital structure solutions are defining the current cycle.

THE PIPELINE: READING THE LEADING INDICATORS

Credit Quality Deterioration Is Accelerating at the Margins

The data paints a picture of a middle market that is stable at the center but fraying at the edges. KBRA’s Q4/25 surveillance of 2,416 unique middle market sponsored borrowers found that multilevel downgrades increased 2.9 times quarter-over-quarter, a sharp acceleration attributed to sponsor and lender support becoming exhausted.1 Downgrades have now outpaced upgrades for two full years, contributing to a growing population of weak borrowers vulnerable to even minor headwinds.

Approximately 12% of borrowers now carry negative cash flow and roughly 13% have interest coverage below 1.0 times — nearly double the 7% to 8% levels observed just one year earlier.2

The Maturity Wall: $1.2T and Counting

Approximately $580 billion of loans in the leveraged loan index and around $625 billion in high-yield bonds mature between 2027 and 2029, representing roughly $1.2 trillion in leveraged debt that must be refinanced or restructured within the next three years.3 As one senior managing director at Houlihan Lokey’s financial restructuring group noted to Octus, an important context for 2026 is the $1 trillion dollars in speculative debt maturities approaching in 2028 — companies, sponsors and lenders are now beginning the process of working through these obligations.4

For the middle market specifically, nearly 30% of companies with debt maturing before year-end 2026 also carried leverage above 10 times or reported negative EBITDA — factors that will intensify refinancing risk.1

The Shadow Default Reality

Perhaps the most significant leading indicator is the growing gap between headline default rates and the true extent of borrower stress. The shadow default rate has more than doubled since 2021.5 KBRA’s review of 2025’s at-risk cohort found that among borrowers that continued to underperform, nearly one-half ultimately defaulted or restructured their capital structures.6

THE EVOLVING RESTRUCTURING PLAYBOOK

LMEs: Five Years In, Still Intensifying

Five and a half years after Serta kicked off the modern liability management exercise era, LME tactics are escalating on both sides. Gibson Dunn’s Scott Greenberg has warned that what companies like Altice USA and KIK Consumer Products executed at the end of 2025 may be early indicators of an even more aggressive playbook in 2026.4

The co-op phenomenon faces new legal scrutiny after corporate borrowers began challenging lender pacts in court. However, practitioners report that litigation risk has not deterred creditors from signing co-ops, even though caution and drafting modifications are expected.4

The Out-of-Court Alternative

For many middle market businesses in significant distress, out-of-court restructuring processes remain viable and often preferable. These processes can be accomplished with less expense and in shorter timeframes while delivering positive outcomes for stakeholders.7 The UCC foreclosure process is gaining attention as an alternative tool that can extinguish secured debt and transfer equity at substantially lower cost than traditional Chapter 11 proceedings.4

Chapter 11: Volume Rising from a High Base

Chapter 11 filings hit a decade-long high in 2025, and multiple forecasters expect a continued increase through 2026.8 PwC emphasizes that without addressing underlying operational problems, balance sheet engineering will only delay and complicate a more disruptive restructuring later.

Sector Concentrations

Consumer Discretionary and Retail: Casual dining chains and consumer products companies face the dual pressure of elevated costs and increasingly price-sensitive consumers.7

Healthcare: Federal budget realignments, tighter Medicaid funding and capital scarcity for early-stage biotech are driving elevated restructuring risk.8

Industrials and Chemicals: Building products, paper and packaging, and chemicals face tariff-driven input cost increases and cyclical demand sensitivity.3

Technology: Non-differentiated tech platforms face margin compression while the AI ecosystem thrives — a K-shaped dynamic driving selective distress.4

Positioning for the Cycle

Restructuring professionals will capture the opportunity by combining sector expertise, capital structure sophistication and relationship capital across the ecosystem. The data is clear: stress is building, tools are evolving and the workflow is expanding. •

1 Q4 2025 Middle Market Borrower Surveillance Compendium, KBRA, Feb. 25, 2026.

2 2026 Turnaround and Restructuring Outlook, Deloitte, 2026.

3 “2026 US Distressed Credit Outlook: Bifurcation, Maturity Wall Promise Busy Year,” PitchBook, Dec. 10, 2025.

4 Zhang, Harvard, “2026 Distressed Outlook: Heated Debtor-Creditor Rivalry, More Change-of-Control Restructuring Due to Failed LMEs, Private Credit Workouts” Octus, Jan. 6, 2026.

5 “Hagerman, Angela, “The Hidden Fault Lines: Understanding Shadow Defaults in Private Credit,” Lexology, Feb. 10, 2026.

6 “Private Credit: Lessons From 2025’s At-Risk Cohort,” KBRA, Feb. 12, 2026.

7 “Duso, Adam & DiNozzi, Robert, “A Workout Without the Mess: When is Article 9 Restructuring the Right Path?” ABF Journal, March 19, 2026.

8Restructuring and Bankruptcy Outlook 2026, PwC, Feb. 4, 2026.

Rita E. Garwood is editor in chief of ABF Journal.