The U.S. middle market manufacturing sector enters 2026 navigating a tariff environment that is simultaneously unprecedented in its complexity, uncertain in its duration and consequential in its impact on financing, deal execution and operational viability. For the dealmaker ecosystem — lenders, sponsors, advisors and attorneys who finance and transact in manufacturing — understanding the current tariff regime and its downstream effects is no longer optional context. It is a core underwriting variable.

The Tariff Landscape: A Multi-Layered Regime

The current tariff environment defies simple characterization because it is the product of multiple overlapping legal authorities, a Supreme Court intervention and rapid policy improvisation. On Feb. 20, 2026, the U.S. Supreme Court struck down all tariffs imposed under the International Emergency Economic Powers Act (IEEPA), which had been the primary authority for the administration’s trade actions.1 The same day, the president signed an executive order imposing a flat tariff on all imports under Section 122 of the Trade Act of 1974 — a time-limited authority that expires after 150 days. The rate was initially set at 10% and subsequently raised to 15%.2

What remains in force is a layered regime that middle market manufacturers must navigate simultaneously: Section 122 tariffs at 15% across a broad import base (expiring mid-July 2026); continuing Section 232 tariffs on steel (25%) and aluminum (25%); and ongoing Section 301 tariffs targeting Chinese goods. Goods compliant with USMCA from Canada and Mexico remain exempt from Section 122, as do products already covered under Section 232.3

Critically, the administration has not conceded the tariff agenda. On March 11, 2026, USTR initiated new Section 301 investigations targeting manufacturing overcapacity across China, the European Union and more than a dozen additional countries — a legal pathway that could allow reimposition of duties similar to the struck-down IEEPA tariffs.2

The Manufacturing Impact: Beyond the Headlines

Margin Compression Is the Central Challenge

For middle market manufacturers, the tariff impact manifests primarily as margin compression rather than demand destruction. Nearly one-third of manufacturers plan to pass all tariff cost increases directly to customers through higher prices, while almost half intend to share costs between pricing adjustments and margin absorption.3 The remaining manufacturers are absorbing costs entirely — a strategy viable only for companies with sufficient margin cushion and balance sheet flexibility.

The cost structure challenge is particularly acute for manufacturers that depend on imported inputs. Brookings Institution analysis found that higher-tech manufacturers — chemical and pharmaceutical makers, transportation equipment producers — import 27% to 33% of their inputs and equipment.4 Tariffs on these inputs function not merely as a consumption tax but as a tax on business investment, reducing competitiveness and putting downward pressure on manufacturing employment. The U.S. shed 8,000 manufacturing jobs in December 2025 alone, with a net loss of 72,000 manufacturing positions between the April 2025 tariff impositions and year-end.4

Working Capital Volatility

The tariff regime’s most insidious effect on middle market manufacturers may be its impact on working capital dynamics. Uncertainty around tariff rates, exemptions and duration is creating inventory management challenges. Manufacturers with adequate storage capacity are gaining strategic advantage during commodity price volatility, purchasing larger quantities when prices dip.3 But for capital-constrained middle market companies, this inventory accumulation strategy requires financing — drawing on revolving credit facilities, stretching payables or seeking incremental ABL capacity.

The USMCA review scheduled for July 2026 introduces additional uncertainty. Manufacturing growth is expected to be essentially flat in 2026, with the sector weighed down by tariff uncertainty and a broader economy that has been sluggish outside the AI sector.5

The Reshoring Calculation

Interest in reshoring has increased, with a growing share of manufacturers actively considering domestic production shifts. However, implementation remains challenging, and many companies are instead seeking alternative trade partners in lower-tariff regions.3 Investment in automation is accelerating as manufacturers seek to offset rising labor and tariff costs through AI-driven production systems and smart manufacturing technologies.3

The Financing Dimension: Tariffs Meet the Credit Cycle

The tariff impact on middle market manufacturing intersects with the broader credit cycle in ways that amplify risk. Deloitte’s 2026 restructuring outlook identifies key stress concentrations in industrials alongside consumer discretionary and healthcare.6 Tariffs drove downstream distress through 2025 via inventory dislocations, rerouting costs, softer demand and procurement disputes, and that pressure is expected to intensify as the financial impact flows through to reported earnings.

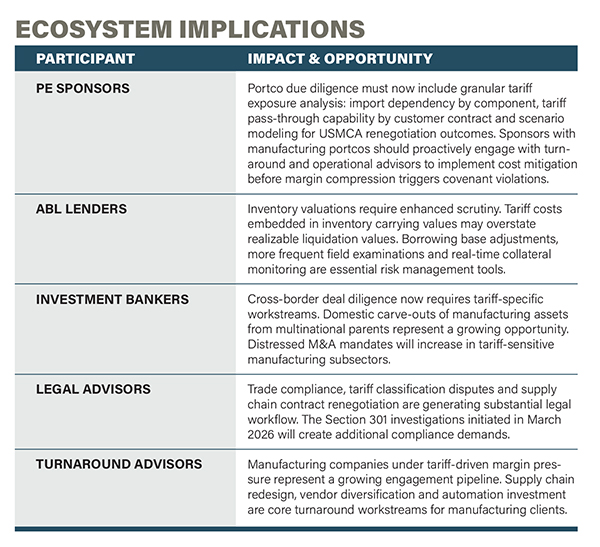

For asset-based lenders, the tariff environment creates a specific collateral monitoring challenge. Inventory values may be inflated by tariff costs embedded in the carrying value of imported goods — creating a distinction between accounting book value and realizable liquidation value that borrowing base calculations must address.

For cross-border M&A, tariffs have moved from the periphery to the center of deal execution. UK and European buyers are now interrogating targets with significant U.S.-facing exports or U.S.-dependent supply chains, running more granular diligence on tariff pass-through models and exposure to further protectionism.7

Sector-Level Analysis: Where Distress Concentrates

Not all manufacturing subsectors face equal tariff exposure. The Yale Budget Lab’s analysis found that tariffs fall most heavily on metal products and electrical equipment, with motor vehicles and apparel also significantly affected.1 In the long run, U.S. manufacturing output may expand by approximately 2% due to tariff protection — but those gains are more than offset by contraction in construction (2.4% decline) and mining (1.1% decline).1

Distressed investors have identified building products, paper and packaging and chemicals as manufacturing-adjacent sectors with elevated restructuring risk in 2026.8

The Path Forward: Navigating Uncertainty

The tariff landscape for middle market manufacturing will remain unsettled through at least mid-2026, with the Section 122 tariff expiration in July and the USMCA review creating binary event risks. The Section 301 investigations could produce new tariff actions by late 2026 or early 2027, ensuring that trade policy uncertainty remains a persistent factor in manufacturing finance and deal execution.

For the dealmaker ecosystem, the imperative is preparation over prediction. Manufacturers and their financial partners cannot control trade policy, but they can build operational flexibility, maintain adequate liquidity buffers, diversify supply chains and structure financing arrangements that accommodate volatile input costs and working capital swings. •

1 “State of Tariffs: February 21, 2026,” Yale Budget Lab,

Feb. 21, 2026.

2 York, Erica & Durante, Alex, “Tracking the Impact of the Trump Tariffs & Trade War,” Tax Foundation, March 13, 2026.

3 “How Tariff Uncertainty and Supply Chain Disruptions Are Reshaping Manufacturing Strategy in 2026,” BMSS / Manufacturing CPA, March 12, 2026

4 Austin, John C., “Not Your Grandfather’s Factory: Why Tariffs Won’t Help Midwest Manufacturing,” Brookings Institution, Jan. 22 2026.

5 Devereux, Mike, “2026 Manufacturing Trends: Adapting to Tariffs and Costs,” Wipfli, November 2025.

6 “2026 Turnaround and Restructuring Outlook,” Deloitte, 2026.

7 “Tariffs and M&A: What to Expect in 2026,” Herbert Smith Freehills, Jan. 14, 2026.

8 Hersch, Jack, “2026 US Distressed Credit Outlook: Bifurcation, Maturity Wall Promise Busy Year,” PitchBook, Dec.

Lisa H. Rafter is publisher of ABF Journal.