Senior Managing Director

Focus Management Group

By Juanita Schwartzkopf, Senior Managing Director, Focus Management Group

Businesses are dealing with a cavalcade of challenges in 2022, not least of all being rising interest rates and inflation. Juanita Schwartzkopf of Focus Management Group provides detailed guidance on how to help borrowers deal with increasing operating expenses and the rising rate environment.

Much of the current discussion and concern regarding the financial performance of businesses has centered on inflation, supply chain problems, labor issues and commodity price fluctuations. These factors certainly put net income performance at risk. This article will explore how to deal with increased operating expenses and examine the impact of increased interest rates on cash flow and loan covenant compliance.

Dealing with Increasing Operating Expenses

Suggestions for dealing with these performance risk problems include the following approaches:

- Price volume variance analysis. Because the per unit prices are changing, it is imperative that volume and price both be considered. For example, fixed and variable operating costs need to be evaluated based on current volumes and prices, not historical levels. A business could make the wrong decision on pricing or expense management if per unit activity is not considered. Often, we use a “common size income statement” as the initial basis for this review. We might consider revenue and expenses per board foot, per pound, per bushel or per some other unit of measure that is specific to the business.

- Customer profitability. The contracts governing the customer relationships need to be reviewed for potential price increases and/or for potential renegotiation at the next opportunity. Understanding the unique customer requirements and the costs associated with providing a product or service will help a business focus on the clients that are the most reliably profitable. A contract summary matrix is the basis for this analysis. Then identifying the unique customer requirements is key. For example, if customer A requires mixed boxes of product and pays the same as a customer that accepts boxes of the same product, the costs to handle and mix the product must be attributed to the profitability of customer A.

- Product profitability. The need to evaluate product and project profitability is critical. Emphasizing more profitable products could shift the break-even performance of a business toward improved performance. The mix between various products that are produced from the same raw materials will also need to be evaluated. For example, chicken processors often say they wish they could purchase a bird with 20 wings to maximize profits.

- Expenses in categories that are experiencing the highest price change need to be evaluated. If transportation and warehousing are up 23% and the business being analyzed has only experienced a 10% increase, it is important to know why the increased costs have not yet been experienced. On the other hand, if the business experienced a 35% increase, that is also critical to expense analysis. For categories such as energy, it may be time to employ an expert in utility cost management and negotiation with alternative energy providers.

- Expenses in categories that rely on providers who rely on transportation and warehousing, energy or food need to be evaluated for price increases and potential further increases. For example, if a supplier is providing an energy intensive material to the business being evaluated, and the cost of the material has not increased at the level of energy increases, it may be time to consider the impact of further price increases.

- Alternative supplier analysis. Businesses that rely on one or two key suppliers are at greater risk of price increases and service disruptions. The emphasis on analysis of alternative suppliers will need to be intensified.

- Labor costs must be evaluated in terms of base pay, overtime, commissions and other incentives paid to employees. Turnover costs must be considered. Remote work versus in-person work requirements need to be evaluated on a person-by-person and department-by-department basis. With labor costs increasing, automation may be a better alternative than it would have been in prior years.

Interest Rate Increases

In addition to operating performance risk from inflation, supply chain problems, labor issues and commodity price fluctuations, the rising interest rate environment not only stresses financial performance, but also puts loan covenant compliance at risk.

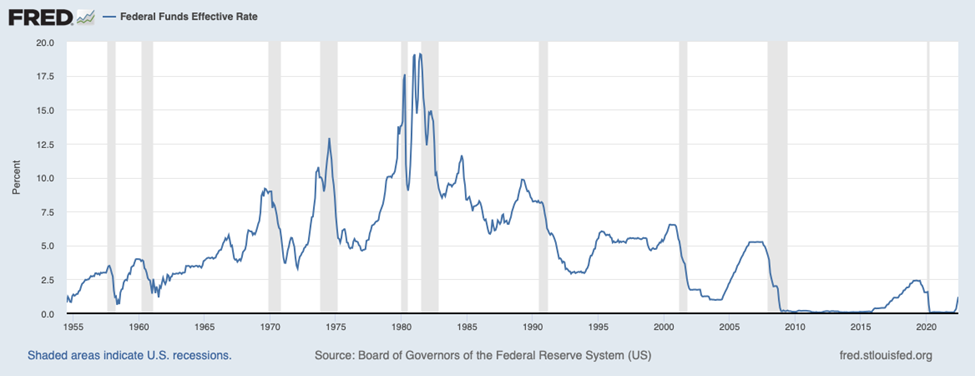

Let’s explore the financial impact of rising interest rates. The last time inflation was at this level was 40 years ago, and interest rate increases were used as a tool to correct for inflation. In the early 1980s, the Federal Funds Rate increased to higher than 19%. Businesses had to deal with the impact of interest rates that exceeded 20% when preparing cash flows and financial forecasts. The chart below shows the Federal Funds Effective Rate from 1955 through 2022.

During the period of high interest rates in the 1980s, businesses did not have the high leverage position many businesses have today.

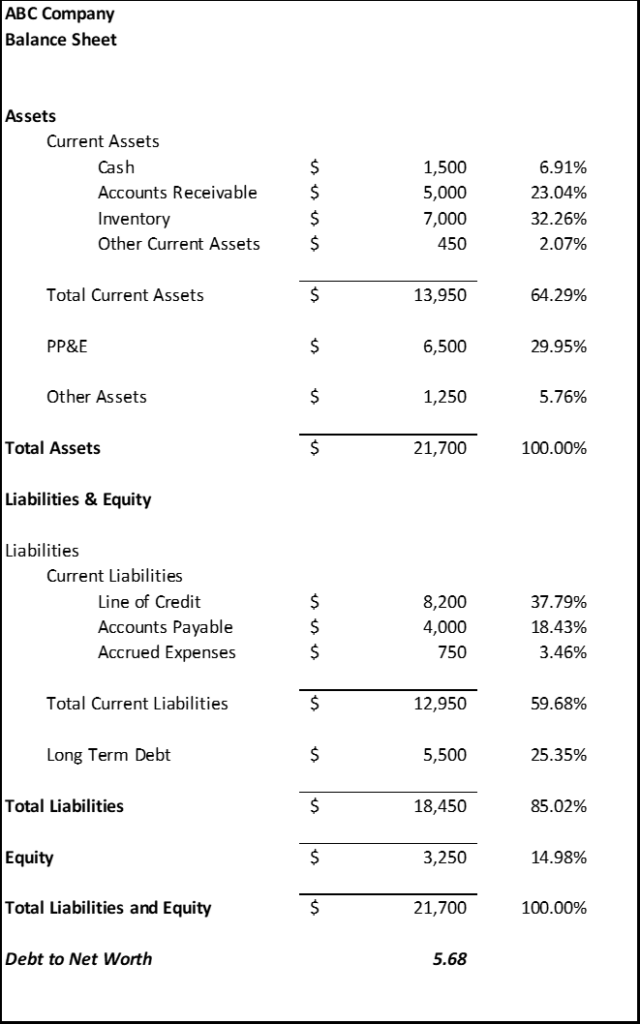

This next table summarizes the balance sheet of a typical company. The company uses a line of credit structure with approximately an 80% advance on accounts receivable and a 60% advance on inventory. The company uses term debt to fund 85% of its net property, plant and equipment. Accounts payable provides cash to support the difference between the accounts receivable and inventory compared to the line of credit outstandings. The debt and capital structure shows a company with a debt-to-net-worth position of 5.68. This is not an unusual leverage position for a company today.

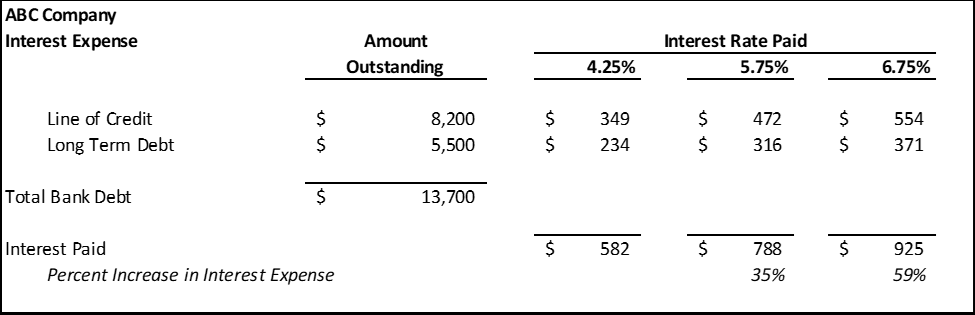

Considering an EBITDA performance level of $1.4 million and interest expense of 4.25%, the company requires $582,000 to pay interest expense. A 1.5% interest rate hike increases interest expense 35% to $788,000, and a 2.5% hike in the interest rate increases interest expense 59% to $925,000.

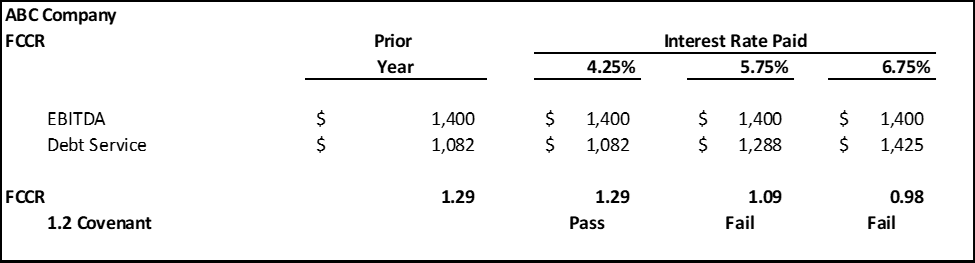

If the company is required to pay $500,000 of principal debt service annually, the 2.5% rate increase will nearly use up the cash available for principal debt service. In the table below, the interest and principal payments under a 1.5% and a 2.5% interest rate increase are compared to the $1.4 million EBITDA performance. With debt service of $1.082 million and EBITDA of $1.4 million, the company has a fixed charge coverage ratio (FCCR) of 1.29.

With a 1.2 FCCR loan covenant, the company would not meet its FCCR covenant if interest rates rise 1.5%, meaning it would not only miss its loan covenant, but would also have insufficient EBITDA to service debt if interest rates rise 2.5%.

With a 1.5% interest rate increase, the company would still be able to meet its debt service requirements, but the amount of cash available to fund increased costs or asset acquisition would be reduced to $112,000. With a 2.5% rate increase, the company would be unable to pay scheduled interest and principal payments.

What Does This Mean?

The increased costs that businesses are experiencing, especially related to labor, warehousing and transportation, energy and food, means companies are feeling EBITDA pressure before the impact of higher interest rates.

Consider that supply chain concerns have meant many businesses have increased their investment in inventory, and coupled with higher prices, that inventory investment increase is both in quantity and in value. If a company requires $10 million of additional inventory and has a 60% inventory advance rate, that company needs to find a source for $4 million of cash to fund inventory increases. Those funding sources could be cash, accounts payable, equity, mezzanine debt or other categories of debt.

Consider the impact of overall cost increases of 10%, which would clearly reduce EBITDA performance by a material level. If a company has expenses of $20 million, a 10% increase in expenses uses an additional $2 million of cash annually. A company generating a 4.5% EBITDA margin on $30 million of sales or approximately the $1.4 million EBITDA noted in the tables above could easily have $20 million of cash expenses that are at risk of increase.

If you combine the working capital pressures, expense increases and interest rate hikes, it becomes increasingly difficult for businesses to successfully perform and to meet loan covenant requirements.

Over the last 12 to 18 months, lenders have seen an increased number of borrowers asking for increases in advance rates and in overall caps on lines of credit. Agreeing to these changes has increased borrowers’ debt levels and puts the ability to service debt at additional risk.

Dealing with the supply chain problems impacts working capital needs and dealing with inflationary pressures increases expenses and reduces EBITDA. Then when layering on the interest rate increases, companies have significant headwinds.

What Can Borrowers and Lenders Do?

Financial analysis often separates the winners from the losers, but in an economic period such as the one we are experiencing in 2022, financial analysis is not a luxury; it is a requirement.

Using a third party to evaluate these key performance metrics may increase the likelihood of success. A third party may be able to prepare the detailed analysis the company is unable to direct resources toward preparing itself. A third party should have fewer preconceived ideas and would be able to look at the data with a clear eye. This is a time to ask tough questions about customers, suppliers and staffing, and consider creative alternatives.

This article first appeared at focusmg.com.

Juanita Schwartzkopf is senior managing director of Focus Management Group.

Schwartzkopf has more than 35 years of experience in commercial banking, business management and financial and management consulting. During her career, she has handled projects involving financing strategies, strategic planning, forecasting, cash management, creditor relationships, information management, bankruptcy, crisis management and business plan development.

Schwartzkopf has held key operating and management positions in many types of companies, from startup to mature businesses. Throughout her career, she has worked on improving performance in severely troubled and stable, healthy companies. She has negotiated lending arrangements on behalf of both creditors and debtors.