Stagnant consumer incomes, explosive growth in online shopping, decreasing popularity of shopping malls and changes in consumption patterns are just a few of the reasons why the retail industry is struggling. While no single factor can take the blame for the turbulence in the industry, the combination has generated stiff headwinds for some retailers and, as a result, bankruptcy cases are steadily on the rise.

Since 2015, more than 12 retailers have filed for Chapter 11, including American Apparel (twice), Eastern Mountain Sports, Fairway, Pacific Sunwear, Quiksilver, RadioShack, Sports Authority, Sports Chalet and Wet Seal. Few of these companies are expected to survive and reorganize; most have been or will be liquidated. And despite a generally improving economy, some observers expect more retail businesses to fail. A recent report published by Fitch identified seven more retailers at high risk of default, including Sears, Claire’s, Nine West, True Religion Apparel, 99 Cents Only, Nebraska Book Company and Rue21.

Lenders need to understand the market pressures that retailers face and how to evaluate their own exposure to this increasingly volatile sector. When retailers seek bankruptcy protection, the results are often bleak. While the Fitch report showed that most first lien lenders did not suffer significant losses in bankruptcy, second lien lenders often did, while unsecured claimants often received little or no distribution. The Fitch report evidence is consistent with other empirical data; few retailers survive bankruptcy intact. While some retailers are sold as operating businesses through bankruptcy sales under §363, retail bankruptcy cases often lead to liquidations.

Stagnant Consumer Incomes

For most of the past decade, consumers have experienced only modest income growth. The table in Figure 1, based on data from the Federal Reserve Bank of St. Louis and the Bureau of Labor Statistics, shows that per capita disposable income has been largely flat. The two sharp peaks are the result of the 2008 tax refund, and at the end of 2012, a spike in sales of capital assets to avoid the tax increase that went into effect in 2013. Despite modest economic growth over the past few years, the compound annual growth rate over the last 10 years has been approximately 1.1%, a level far below the post-World War II average of nearly 3%.

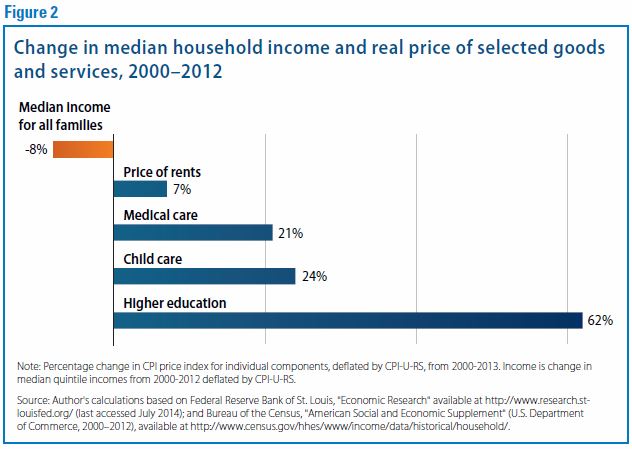

In addition, consumers have faced increased costs for housing, medical care, child care and education, (Figure 2).

The combination of stagnant disposable income and increased costs has made consumers cautious about spending. Retailers have reported that the outlook is soft this year. Just 49% of U.S. retail chains said sales at established locations rose in Q2/16 compared to a year earlier, according to an analysis of 110 companies by research firm Retail Metrics. That marks the lowest percentage for any quarter since 2009, when the U.S. was recovering from the 2008 global financial crisis. Sales growth has been stuck in a 1% to 2% range, according to Retail Metrics, which is in line with the weak growth in consumer income.

Rise of Internet Retailing

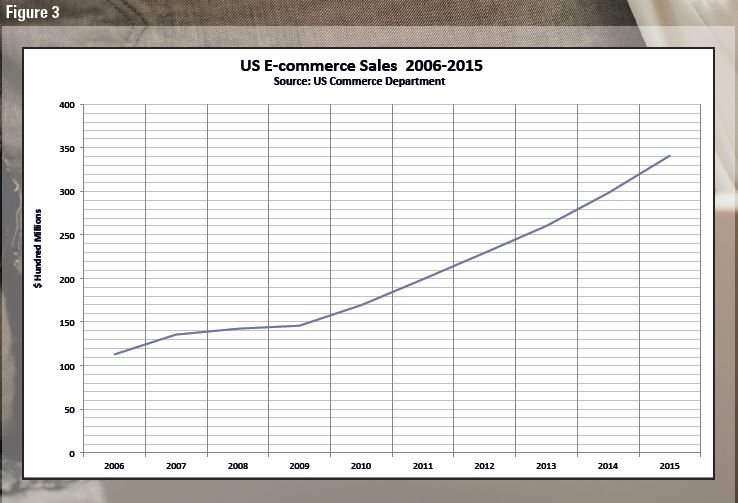

The continued growth in e-commerce, as shown in Figure 3, has also contributed to retail store weakness. Online retail sales nearly doubled from 2005 to 2014, and while most retailers have adopted some form of internet sales platform, analysts say that e-commerce growth has come at the expense of brick-and-mortar stores. The rise is expected to continue as sales from mobile phones and tablets further accelerate the trend away from store sales.

The popularity of online shopping has also contributed to the decline of shopping malls, which is exacerbated by the flagging fortunes of the department stores that were the malls’ traditional anchors. According to a report by retail analyst Green Street Advisors, Macy’s, Nordstrom, JCPenney, Sears and other department stores have seen in-store sales per square foot decline 24% since 2006.

In response, many department stores have announced plans to close stores in 2017: JCPenney will turn off the lights at seven locations, Macy’s will close 100 stores and Sears expects 150 closures, including 109 Kmart stores. Shopping malls depended on these anchor stores to generate traffic that drew shoppers to the other in-line stores. As traffic diminishes at those anchors, the in-line stores will see reduced shopper volume.

Changing Consumption Patterns

Changes in consumer spending patterns have also contributed to the decline. A generation ago, clothing purchases comprised between 5% and 6% of consumer expenditure, compared to only 3.5% before the Great Recession. That reduction is continuing, according to data from the Bureau of Labor Statistics, aggregate household spending on clothing has declined by nearly 10% since 2005.

One reason for this decline, according to MasterCard executive Sarah Quinlan, is the increase in casual attire in the workplace. “It’s not that consumers aren’t buying any clothing, but with relaxed workplace dress codes, priorities and styles have changed. One wardrobe is all that person needs,” she says.

Also, according to Marshal Cohen, chief industry analyst at The NPD Group, “There’s less focus on image and apparel and more focus on electronics. The millennial and post-millennial is very focused on being connected. Getting connected is already costing hundreds of dollars per month. That used to buy jeans. It’s not buying jeans anymore.”

In addition to electronic gadgets, Americans are spending more money on travel and restaurants. According to the U.S. Travel Association, Americans were projected to spend $802 billion in 2015 on leisure travel, and spending on travel has risen 14.5% since 2011, according to a report by MasterCard. Restaurants have also benefitted. Sales at restaurants open at least a year have consistently outperformed retail same-store sales, according to Thomson Reuters.

Retail Bankruptcy Results

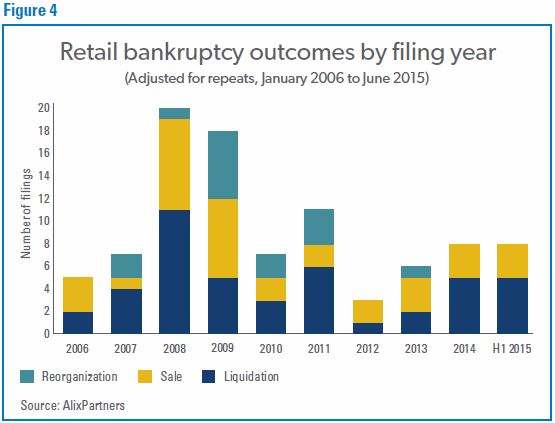

In this era of change in the retail environment, it is not surprising that retail bankruptcies are increasing, although few retailers that file for Chapter 11 survive and reorganize. According to a 2016 study by turnaround consultants AlixPartners, 55% of all retail cases result in liquidations. There are two other notable trends in the AlixPartners data: the huge spike in retail cases in 2008 and 2009 and the steady increase in cases since 2012.

The following are summaries of the outcomes in some recent retail bankruptcy cases, which are consistent with the results shown in Figure 4:

- Sports Authority: Sold intellectual property to competitor Dick’s Sporting Goods for $15 million, closed 450 stores and liquidated leases and inventory

- Wet Seal: Closed 340 stores, sold 140 stores and inventory to Versa Capital Management for $7.5 million

- Hancock Fabrics: Closed 250 stores, sold intellectual property to competitor Michael’s Stores for $1.3 million and liquidated leases and inventory

- RadioShack: Closed approximately 2,300 stores and sold assets to Standard General for approximately $170 million in cash and credit bid. Standard General will operate approximately 1,700 stores.

- Caché: Sold its inventory to Great American for $18 million, closed 218 stores and sold some leases

- Aeropostale: Sold its assets to a consortium of inventory liquidators and two of its major landlords for $243 million. Prior to Chapter 11, operated approximately 800 stores in the U.S. and Canada. New owners may operate as many as 500 stores, but they are still in the process of evaluating locations.

Challenges to Reorganization

Retailers experience high rates of liquidation because they typically have very little time to execute a reorganization or sale. Prior to the 2005 amendments to the Bankruptcy Code, retailers often spent two or more years in bankruptcy. During that time, they used a variety of strategies to fix their businesses, including merchandising changes and evaluation and/or closure of marginal stores. They typically had one or more holiday seasons in which to test the changes. But the 2005 amendments to the Bankruptcy Code substantially shortened that timeline, effectively giving retailers only a few months to obtain approval for a sale or reorganization before getting forced into liquidation. Coupled with the changes in the Bankruptcy Code was an increased willingness of bankruptcy judges to approve DIP financing agreements that had strict timetables for retailers to confirm a plan or commence liquidation.

The biggest change to the code came in §365(d)(4), which now provides a maximum of just 210 days before unassumed store leases are deemed assumed — absent individual landlord approvals. Rejecting a lease before it is assumed creates a general unsecured claim, whereas rejecting a lease after assumption creates an administrative claim. Thus, senior lenders will typically impose a timeline in cash collateral or DIP financing orders that ensures all unwanted leases get rejected well in advance of the 210-day deadline. Because it can take up to 90 days to run store going-out-of-business sales, senior lenders frequently attempt to mandate a decision on whether to liquidate or reorganize a debtor within 120 days of the filing.

Lenders have another incentive to push liquidation: strong results from inventory liquidations. Inventory can make up as much as 50% of a typical retailer’s assets. In several recent cases, the inventory liquidation values were at or above 100% of the debtor’s cost. Lenders are aware that liquidators have achieved these returns, lessening the fear that a liquidation will adversely affect them. Because liquidation offers lenders a high probability of a good result and the certainty of an accelerated timeline, they are less likely to give retailers time to reorganize. Negotiating and obtaining confirmation of a plan of reorganization can be time consuming, and if the pre-petition lenders are not cashed out, they remain exposed to the debtor. Thus, lenders have incentives to push liquidation.

Another important 2005 change to the Bankruptcy Code was the introduction of §503(b)(9), which gives administrative priority status to vendor claims for the value of goods sold in the 20 days immediately preceding a bankruptcy filing. Unless trade creditors agree to less favorable treatment, a retailer has to have cash at confirmation to pay for those goods in full to confirm a plan of reorganization because administrative-priority claims must be paid in cash on the effective date of a plan. This change significantly increases the cash cost of a reorganization plan.

Lender Strategies for Struggling Retailers

Given the ongoing forces that are affecting the retail sector, lenders may face exposure to one or more troubled borrowers. Retailers rarely experience catastrophic failures; they typically struggle financially long before they seek bankruptcy relief. During that time, it is common for them to experience either technical or financial defaults under their lending agreements. The default gives a lender the opportunity to reconsider the terms under which it is doing business with its borrower, to anticipate the possibility of still further defaults and to develop an overall strategy for being paid in full. Deciding which responses are appropriate will depend on many factors, including the length of the relationship with the borrower, the lender’s assessment of management and the lender’s assessment of recovery in full in the event of a bankruptcy.

A loan default is the best opportunity for a lender to reconsider the core terms of its lending agreement. Do the financial covenants make sense at their current levels? Are there other positive or negative covenants that need to be added? On a structural level, the lender needs to consider the nature of the default and the likelihood of additional defaults in the near term. The lender should consider trends in the borrower’s sales and profitability and how the debtor compares with peer retailers. The lender should assess the quality of the borrower’s market strategy and management team. In addition, lenders need to analyze their likely payout from an orderly liquidation of the borrower’s business. Another key variable is the remaining tenor of the loan. How likely is it that the borrower will be able to refinance its debt when due?

Because each retailer faces its own market, customer base, vendor base and geographic footprint, there are no cookie-cutter solutions. A loan default is the best opportunity for a lender to reconsider the core terms of its lending agreement. Do the financial covenants make sense at their current levels? Are there other positive or negative covenants that need to be added? On a structural level, the lender needs to consider the nature of the default and the likelihood of additional defaults in the near term. For more troubled companies, lenders can require that a borrower retain a chief restructuring officer acceptable to the lender or that the borrower retain an investment bank and begin the process of marketing the company for sale. Lenders need to calibrate their responses to the facts of each case; a minor covenant failure does not necessarily mean that a lender should seek a change in management. But if the borrower has shown a pattern of declining sales and/or profitability, good lending practice suggests that the lender act to protect its interests before the borrower experiences an irreversible decline.